The 2004 EU Enlargement Was a Success Story Built on Deep Reform Efforts

|

(Credit: legna6/iStock by Getty Images)

Poland is one of the success stories of European economic convergence. The country, which in January takes the reins of the Council of the European Union (the decision-making institution representing the Union’s member states) is now the EU’s sixth largest economy. This convergence process was driven by the 2004 EU enlargement, which also welcomed the Czech Republic, Cyprus, Estonia, Hungary, Latvia, Lithuania, Malta, Slovenia, and Slovakia into the Union, expanding the EU’s population by about 20 percent.

Twenty years later, as new EU accession discussions are underway, it is worth looking at how much the earlier enlargement benefitted new members and the whole Union, and reflect on the economic returns of broadening the European single market. The current accession candidates, in different stages of the process, are Albania, Bosnia and Herzegovina, Kosovo, Montenegro, North Macedonia, Serbia, Georgia, the Republic of Moldova, Ukraine and Türkiye. In October, the European Commission issued a new report with detailed assessments of the state of play and the progress toward EU accession made by each candidate.

|

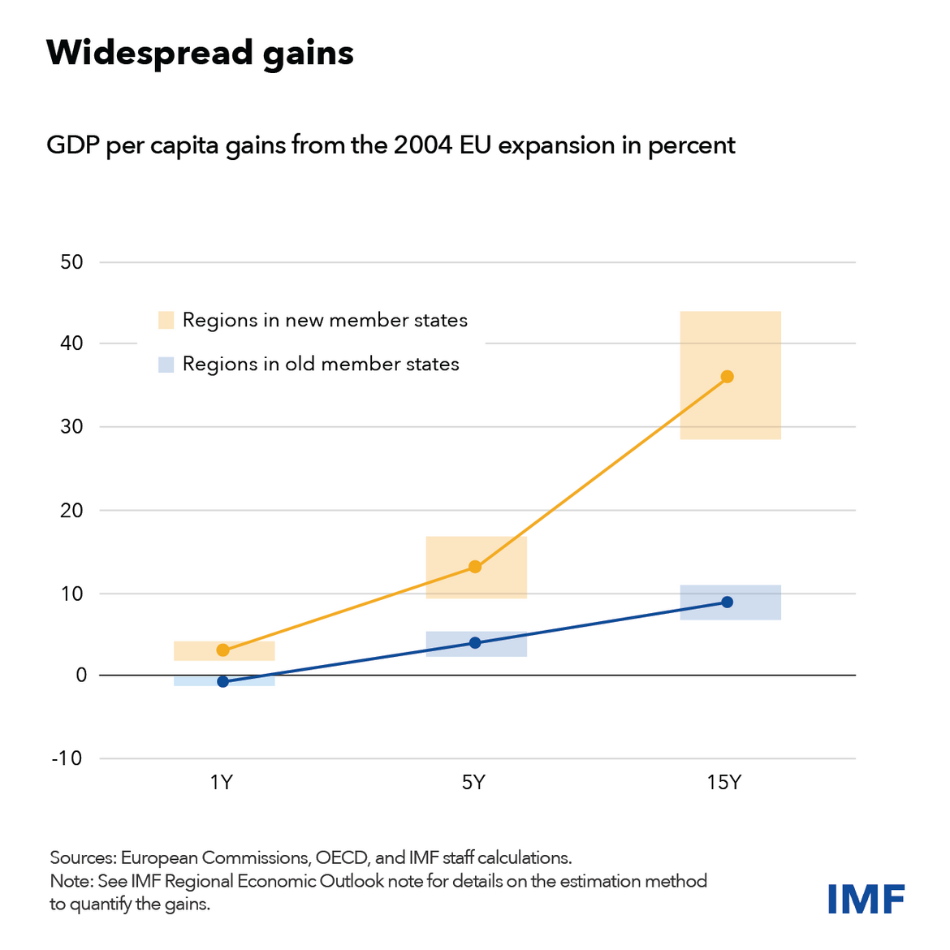

A new note by the Regional Economic Outlook for Europe shows that the 2004 EU enlargement brought substantial income gains. These gains were particularly large in the new member states: after 15 years GDP per person was on average more than 30 percent higher than it would have been without EU accession.

The factors driving these gains in new members were threefold. First, the 2004 group benefitted from more comprehensive economic reforms prior to joining the EU than implemented in comparable other regions, including on trade, financial sector, and product market liberalization. Second, additional financing from foreign direct investment and EU cohesion funds helped boost the capital stock. Third, technology transfers and enhancements in educational attainment improved productivity.

While all regions in new EU countries gained, some gained more than others. Those already better integrated into value chains with the existing member states increased GDP per person nearly 10 percentage points more than those less integrated pre-accession, irrespective of geographic distance. Regions with firms that had easier access to long term financing gained close to 15 percentage point more than others.

Existing member states benefitted from EU enlargement too. By 2019, income per person was around 10 percent higher than it would have been in a scenario without enlargement. The main driver of these gains was the expansion of the EU’s single market, which allowed firms to expand production and reap efficiency gains, including through higher investment in the accession countries. While regions in Scandinavia, Germany, and Austria—already well integrated with new member states prior to accession—gained the most, many regions further away benefitted too.

What does this mean for next wave of EU accession? A key lesson is that both accession candidate countries and existing EU members can benefit if they put in the work. This is no easy task. It would require strong pre-accession reforms, significant financing, political resolve, and possible institutional adaptation.

Some factors of the 2004 successes may be harder to achieve today. For accession countries this puts a premium on those actions directly under their control, such as the reform effort to close business regulation and institutional gaps to the EU. From the existing members’ side, continuing to deepen the single market by removing remaining within-union trade barriers and advancing the capital market union to finance dynamic firms’ growth would further amplify the potential gains. These joint efforts could not only accelerate catch-up within Europe, but also help narrow Europe’s persistently large income gap with the US.