Previsões econômicas do FMI para 2025 e mais além: crescimento moderado, mais divergências entre principais economias - IMF blog

| |||||

|

Previsões econômicas do FMI para 2025 e mais além: crescimento moderado, mais divergências entre principais economias - IMF blog

| |||||

|

Não há “milagre” que dure para sempre; ou melhor, o ritmo do crescimento econômico é sempre mais alto em economias que saem de muito baixo (mas com politicas corretas); depois fica mais difícil. Mas tem muito país pobre que permanece estagnado na pobreza, alguns até recuam, pois são ditaduras predatórias. Acontece até com quem era rico. Venezuela, por exemplo!

Talvez você tenha lido alguma notícia sobre a crise migratória na fronteira dos Estados Unidos com o México. Mas eu duvido que o leitor consiga adivinhar a nacionalidade que teve mais crescimento no número de detenções migratórias: os chineses.

Ao fim de 2023, o número de imigrantes chineses detidos na fronteira era quase 600% maior do que no mesmo período do ano anterior. Mas como há um crescimento percentual tão forte no número de pessoas que estão saindo de um país que está a 11 mil quilômetros para imigrar por terra? Eu, que moro nesta fronteira, também me fiz essa pergunta.

Quase todos eles, ao cruzar, pedem asilo político — e vão ter seu caso julgado pelas autoridades migratórias. Mas os chineses, vindo de uma ditadura, têm uma probabilidade muito maior de sucesso em seus casos. Em 2021, 17% dos pedidos de asilo de mexicanos foram aceitos. Entre os salvadorenhos, o percentual sobe para 28%. Entre chineses a taxa foi de 81%.

A probabilidade de sucesso torna a arriscada viagem um pouco mais atrativa. Para muitos deles, ela começa no Equador (país que não exige visto para chineses) e segue por terra cruzando Colômbia, América Central, até a fronteira Norte do México.

Existem fatores políticos e tecnológicos que podem ajudar a explicar esse incremento no fluxo.

Há um aumento na repressão política. Políticas recentes incluem interferências sem precedentes em universidades, prisão de advogados de defesa e repressão a protestos em províncias como Hong Kong. Ao mesmo tempo, à medida que as tensões entre EUA e China têm aumentado nos últimos anos, o acesso a vistos de turismo para chineses tem se tornado mais limitado.

Na esfera tecnológica, a conhecida censura do governo hoje tem implementação mais difícil. Com o uso de softwares de redirecionamento de rede, muitos chineses têm acesso à mídia social ocidental. Entre aqueles que chegaram nos Estados Unidos, muitos relataram ter aprendido sobre o trajeto da viagem no Instagram e no TikTok (ou seus equivalentes chineses).

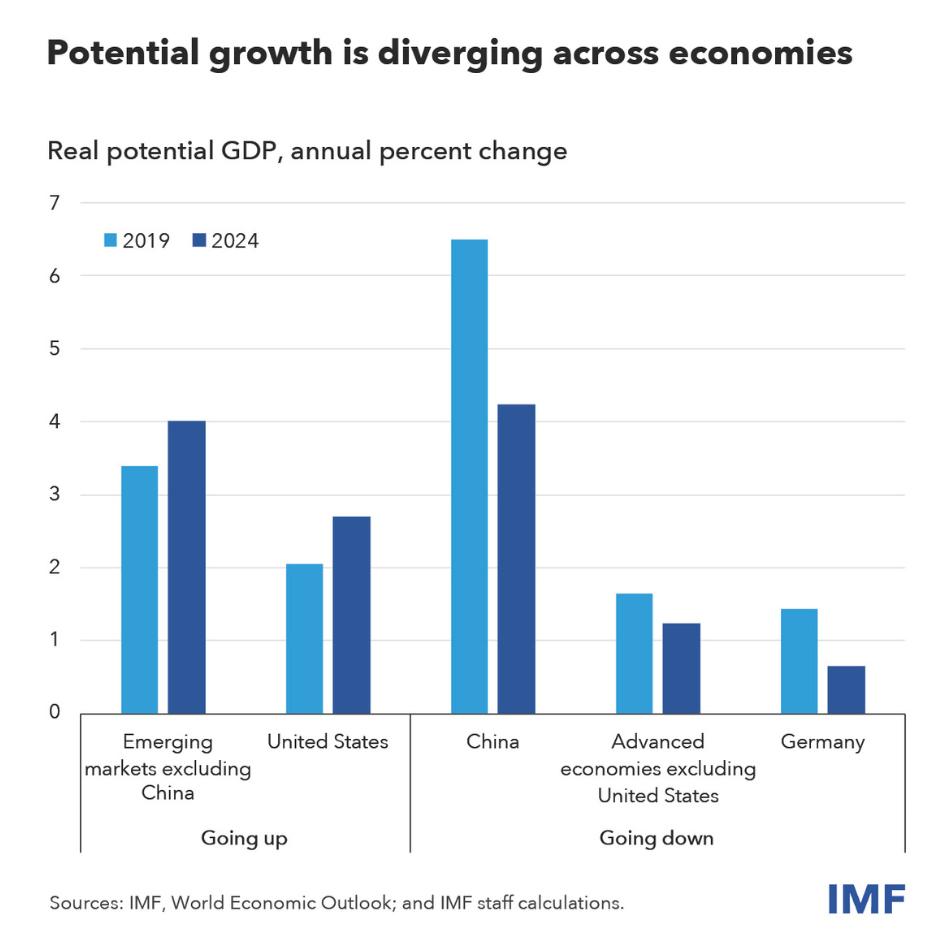

Igualmente importante, há muitos fatores econômicos que ajudam a explicar esse tipo de fluxo migratório. Durante décadas, nos acostumamos a ver a economia chinesa crescendo a 10%. Mas a partir da década passada, a trajetória começou a arrefecer, com taxas rondando os 6%. Recentemente, o crescimento chegou a ficar abaixo dos 3% e o FMI prevê que nos próximos anos deve ficar entre 3-4%.

Como consequência, as projeções futuras de quando a economia chinesa ultrapassará a americana têm sido revisadas para o futuro. Por exemplo, em 2021 o FMI previa que a economia chinesa seria, no ano passado, 76% do tamanho da economia americana. Na verdade, com o crescimento mais baixo, ela chegou em 2023 com 65% da economia americana.

A previsão mais recente é que nem mesmo em 2028 vá se alcançar os 72% citados anteriormente. Alguns institutos privados já preveem que a economia chinesa nunca vá alcançar o tamanho da economia americana!

Em parte, a explicação é demográfica. A população americana continua expandindo, por causa do fluxo constante de imigrantes. Já a população chinesa tem envelhecido e estagnado em tamanho, muito em função da política de filho único ali existente.

Mas também há uma desaceleração no crescimento da produtividade do trabalho na China.

Isso não deveria ser uma surpresa tão grande. Um dos mais influentes economistas do século passado, Robert Solow, ganhou o Nobel principalmente por uma teoria do crescimento que previa que países mais pobres (com menos capital acumulado) tenderiam a crescer mais rápido do que aqueles com muito capital.

O Brasil também passou por seu milagre do crescimento. Hoje a China tem uma renda per capita próxima ao brasileiro. A dúvida que fica é se, como nós, eles também vão cair na “armadilha da renda média” — quando um país sai da pobreza e em seguida para de crescer. Num país em que tem taxas de poupança muito altas, infraestrutura bem melhor que a nossa e excesso de estoque de imóveis, é difícil pensar em avenidas tradicionais para estimular o crescimento.

E isso se reflete do outro lado do mundo. Muitos dos jovens chineses que cruzaram a fronteira falaram a repórteres que saíram da China porque hoje está muito mais difícil encontrar emprego. Para eles, chegou ao fim o milagre chinês. A pergunta mais importante é: e para os chineses, muito mais numerosos, que ficaram em casa? O que o futuro reserva?