| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||

As projeções de alguns economistas sobre um Bretton Woods III são, como diria Mark Twain, altamente exageradas. O dólar parece destinado a servir de moeda internacional, para reservas nacionais, para os intercâmbios globais, durante muitos anos mais.

The US dollar might slip, but it will continue to rule

The international monetary system may be at the threshold of significant change from a combination of economic, geopolitical, and technological forces. But it is an open question whether these forces will knock the US dollar off its pedestal as the dominant international currency, which it has been for much of the post–World War II period. How these forces play out will have major ramifications for the evolution of the world order, because financial power is a key element of soft power.

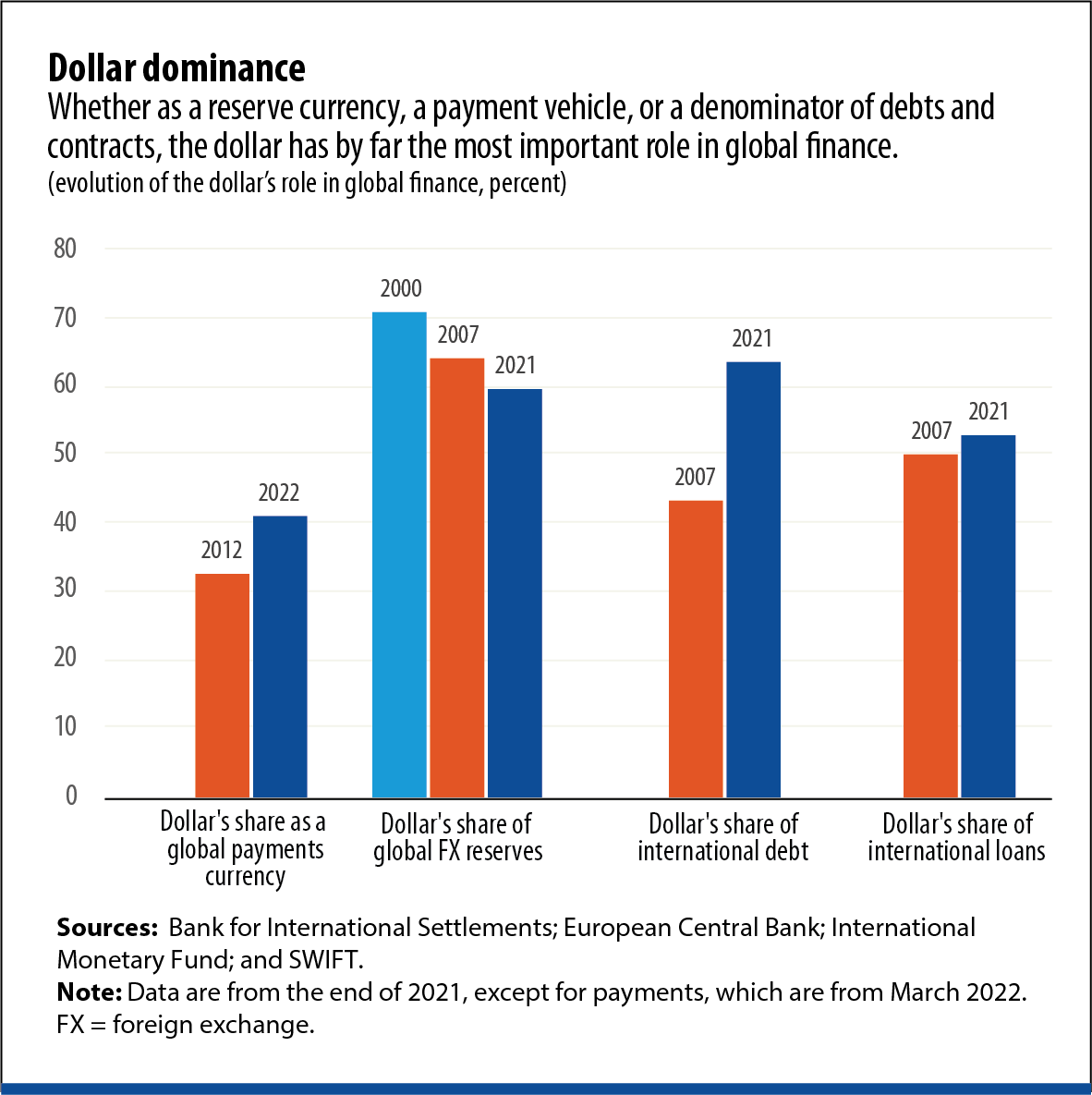

The dollar dominates every aspect of global finance. Nearly 60 percent of the world’s central banks' foreign exchange reserves, essentially their rainy-day funds, are invested in dollar-denominated assets. Almost all commodity contracts, including those for oil, are priced and settled in dollars. The dollar is used to denominate and settle a majority of international financial transactions (see chart).

The preeminence of the dollar gives the United States considerable power and influence. Because transactions entailing use of the dollar invariably involve the US banking system, the US government can severely punish countries, such as Iran and Russia, by imposing sanctions that limit their access to global finance. It also means that the fiscal and monetary policies of the US government affect the rest of the world because they influence the value of the dollar. And it allows the United States to punch well above its weight in global GDP and trade, which has long rankled US rivals and allies alike.

Changes are underway that could undermine this supremacy.

Raw US economic dominance is shrinking. The US economy now accounts for about 25 percent of global GDP (at market exchange rates), down from 30 percent in 2000. Indeed, the locus of economic power, as measured by the share of global output and trade, has been shifting toward emerging market economies, led by China, for more than two decades.

The emergence of digital currencies, both private and official, is shaking up domestic and international finance. Consider international payments. They involve multiple currencies, payment systems operating on diverse protocols, and institutions governed by varying regulations. As a result, cross-border payments have tended to be slow, expensive, and difficult to track in real time. New technologies spawned by the cryptocurrency revolution now make for cheaper and practically instantaneous payment and settlement of transactions.

Even central banks are getting into the game, using the new technologies to increase the efficiency of payment and settlement mechanisms for cross-border transactions by their domestic financial institutions. The central banks of China, Hong Kong SAR, Thailand, and the United Arab Emirates are collaborating on one such effort, and other central bank consortia are engaged in similar exercises.

These developments will alleviate payment-related frictions in international trade, because quicker settlement reduces risks from exchange rate volatility. Exporters and importers will enjoy less need to hedge against the risks of exchange rate volatility that stem from long delays in processing and finalizing payments. Economic migrants sending remittances home, a key source of revenue for many developing economies, will also benefit from lower fees.

Changes are also afoot in foreign exchange markets. For example, transactions between pairs of emerging market currencies are becoming easier as financial markets and payment systems mature. Typically, converting such currencies to dollars, and vice versa, has been easier and cheaper than exchanging them for one another. But China and India, for example, will soon no longer need to exchange their respective currencies for dollars to conduct trade cheaply. Rather, exchanging renminbi for rupees directly will become cheaper. Consequently, the reliance on “vehicle currencies,” particularly the dollar, will decline.

In short, as international payments become easier and perhaps even increase in volume as frictions recede, the role of the dollar in intermediating such payments could decline. In tandem with these changes, the dollar’s primacy in the denomination of various transactions will decline. Pricing of oil contracts in dollars is less important, for example, if China can use renminbi to pay for its oil purchases from Russia or Saudi Arabia.

Digital technologies affect other aspects of money. With the rapid decline in the use of cash, many central banks are moving forward—or at least experimenting—with central bank digital currencies (CBDCs). China, among major economies, is well into advanced trials of its CBDC.

The prospect of a digital renminbi available worldwide has intensified speculation that China’s currency could gain in prominence and perhaps even rival the dollar. But a digital renminbi by itself will not shift the balance of power among major currencies. After all, most international payments are already digital. Rather, it is China’s Cross-Border Interbank System (CIPS), which can communicate directly with other countries’ payment systems, that will enhance the renminbi’s role as an international payment currency.

Even so, the renminbi still lacks some key attributes that reserve currencies typically need to be considered reliable stores of value. China has made some progress in this area—removing restrictions on cross-border capital flows, leaving its currency’s value to market forces, and broadening foreign investors’ access to its bond markets. But the government has rejected institutional changes essential to garnering the trust of foreign investors, including an independent central bank and the rule of law. Indeed, China is alone among reserve currency economies in not sharing these characteristics.

Still, the renminbi has made some progress as an international currency. By some measures, it is used for about 3 percent of international payment transactions, and about 3 percent of global foreign exchange reserves are held in renminbi. Such measures of renminbi prominence will almost certainly increase as the Chinese economy and its financial markets grow and foreign investors, including central banks, allocate a greater portion of their portfolios to renminbi-denominated assets—if for no reason other than diversification. But it is unlikely that the renminbi will pose a serious threat to the dollar’s dominance unless the Chinese government embraces both market-oriented economic reforms and upgrades to its institutional framework.

The new technologies will both help and hinder emerging market economies, with collateral effects that—coupled with other developments—in the end may enhance dollar dominance rather than erode it.

On one hand, as mentioned earlier, new financial technologies will improve access to global financial markets for firms and households in emerging market and developing economies. Reduced frictions in international payments will enable these economies’ firms to gain access to global pools of capital and give their households easier access to opportunities for international portfolio diversification—permitting better returns on their savings while managing risk.

On the other hand, the proliferation of conduits for money to flow across national borders will intensify developing economies’ vulnerability to the vagaries of major central banks’ policies and the whims of domestic and international investors. It is also likely to render capital controls less effective. Even cryptocurrencies such as Bitcoin have been channels for capital flight when a country’s currency is collapsing and domestic investors lose faith in their country’s banking system. In short, greater capital flow and exchange rate volatility will further complicate domestic policy management, with deleterious consequences for economic and financial stability in these economies.

The natural response of policymakers in emerging markets is to protect their economies against such outcomes by further expanding their stocks of hard currency foreign exchange reserves. But Russia’s loss of access to the bulk of its foreign exchange reserves—the result of Western sanctions imposed in response to its invasion of Ukraine—shows that such buffers might be unavailable in times of dire need. This has generated speculation that emerging market economies will look to other reserve assets—such as gold, cryptocurrencies, or the renminbi—as alternatives to government bonds issued by advanced economies.

The reality, though, is that assets such as gold are not viable alternatives because their markets are not liquid enough; it would be difficult to sell a large stock of gold within a short period without setting off a plunge in gold prices. Cryptocurrencies such as Bitcoin have the additional problem of being highly unstable in value. Even renminbi reserves might be of limited help because that currency is not fully convertible.

For the foreseeable future, there is likely to be strong and perhaps even rising demand for “safe assets” that are liquid, available in large quantities, and backed by countries with trusted financial systems. There are limited supplies of such assets, and the US dollar—which represents a powerful combination of the world’s largest economy and financial system, backed by a strong institutional framework—remains the dominant supplier. The desire for diversification has led to recent modest increases in the shares of Australian, Canadian, and New Zealand dollars in global foreign exchange reserves, but these—and other leading reserve currencies, such as the euro, the British pound, and the Japanese yen—have only marginally dented the US dollar’s share.

Changes coming to the international monetary system pose additional threats to the currencies of smaller and less developed economies. Some of these countries—especially those with central banks or currencies that lack credibility—could be overrun by nonnative digital currencies.

It is possible that national currencies issued by their central banks, particularly currencies seen as less convenient to use or volatile in value, could be displaced by stablecoins—private cryptocurrencies issued by multinational corporations or global banks and usually backed by US dollars to maintain stability—or by CBDCs issued by major economies. Even a volatile cryptocurrency such as Bitcoin might, in addition to enabling capital flight, be preferred to the local currency during economic turmoil.

But it is more likely that economic turmoil would result in further dollarization of economies, particularly if digital versions of such well-known currencies as the dollar become easily available worldwide.

Although digital technologies enable new forms of money that could challenge fiat currencies and set off a new era of domestic and international currency competition, it is equally likely that these new forces will create more centralization, with some currencies accreting even more power and influence. In other words, many of these changes might reinforce rather than weaken the dollar’s dominance.

There are other forces that sustain the dollar’s dominance, especially the prospect of losses were the dollar to falter. Foreign investors, including central banks, hold nearly $8 trillion in US government debt. Overall US financial obligations to the rest of the world total $53 trillion. Because these liabilities are denominated in dollars, a plunge in the value of the dollar would make no difference to the amount the United States owes but would reduce the value of those assets in terms of the currencies of the countries that own them. China’s holdings of US government bonds, for instance, would be worth less in renminbi.

On the flip side, US investors’ holdings of foreign assets, about $35 trillion, are denominated almost entirely in foreign currencies. Hence, an increase in the value of those currencies relative to the dollar would mean that they are worth more when converted into dollars. Thus, although the United States is a net debtor to the rest of the world, a fall in the value of its currency would result in a windfall to the United States and a big loss to the rest of the world. For the foreseeable future, then, even dollar detractors might fear a sharp fall in its value, leaving the world stuck in a “dollar trap.”

The upshot is that the dollar’s role as the dominant reserve currency will likely persist, even if its status as a payment currency erodes, which itself is uncertain.

A likelier prospect is a reshuffling of the relative importance of other currencies while the dollar retains its primacy. Rather than knocking the dollar off its pedestal, new technologies and geopolitical developments might entrench its position.

ESWAR PRASAD is a professor at Cornell University and a senior fellow at the Brookings Institution.

Norway has announced that it will from now on use the name “Belarus” instead of “Hviterussland” (literally “White Russia”) in all official documents. The move is seen as a symbolic snub to Russia and recognition of Belarus’s aspirations to emerge from the Kremlin orbit and embrace democracy. “We believe it is right to change the use of names in solidarity with the Belarusian democratic movement,” commented Norwegian Prime Minister Jonas Gahr Støre.

Norwegian Foreign Ministry officials underlined the symbolic importance of the switch and stressed the need to emphasize the difference between Belarus and Russia.

Norwegian Minister of Foreign Affairs Anniken Huitfeldt first broke the news of the name change in a personal call with the exiled leader of Belarus’s democratic opposition, Sviatlana Tsikhanouskaya (pictured), on the eve of this year’s International Day of Solidarity with Belarus, which is marked annually on May 29. “Although there are both historical and linguistic arguments for writing “Hviterussland,” it is ultimately a political issue,” stated Huitfeldt. “We do this as a sign of solidarity with the Belarusian democratic movement. They will not be a continuation of Russia.”

Belarusian opposition leader Sviatlana Tsikhanouskaya welcomed the Norwegian gesture, which she praised as “more than just symbolic.” Belarusian journalist Hanna Liubakova shared this sentiment, commentingthat she saw Norway’s step as a sign of growing international recognition that referring to modern Belarus as “White Russia” was anachronistic and misleading.

Subscribe for the latest from BelarusAlert

Receive updates for events, news, and publications on Belarus from the Atlantic Council.

Norway’s decision to begin using the name Belarus in official documents is part of a regional trend, with fellow Scandinavian countries Sweden and Denmark also making similar switches from their own outdated versions of “White Russia” in recent years. This reflects broader changes in international perceptions of the country following a 2020 pro-democracy uprising that thrust Belarus into the global headlines following decades spent in the post-Soviet shadows.

For much of the post-Soviet period, Belarus was perhaps best known internationally as the last dictatorship in Europe. It owed this dubious honor to Belarusian President Alyaksandr Lukashenka, who won election in 1994 before proceeding to dismantle the country’s fledgling democracy and reestablish a Soviet-style one-party state.

For over a quarter of a century, Lukashenka was able to successfully suppress all domestic opposition and strengthen his grip on power while maintaining close ties with neighboring Russia. He faced the first serious challenge of his entire reign in August 2020 when heavy-handed attempts to rig the country’s presidential election served as a focal point for simmering public frustrations, leading to the eruption of mass protests across the country on the evening of the vote.

This pro-democracy protest movement gained momentum in subsequent weeks and caught the world’s imagination. It dominated international news coverage for much of late summer and early fall 2020, with many seeing the unprecedented people power uprising as the latest chapter in the slow-motion collapse of the Soviet Empire. The Lukashenka regime looked destined to fall until Russia intervened with a financial lifeline and a promise to send in the Russian security services if necessary.

Lukashenka has remained entirely dependent on Russian support ever since. In return, he has gradually surrendered his country’s sovereignty to the Kremlin, allowing Moscow to expand its political, economic, and military footprints in the country. In February 2022, Lukashenka permitted Putin to use Belarus as a platform for the invasion of Ukraine. Thousands of Russian troops flooded across the Belarusian border into Ukraine as part Putin’s failed attempt to seize Kyiv. The country has also served as a launch pad for the bombardment of Ukrainian towns and cities.

O Brasil retrocedeu 50 anos, meio século, na temática ambiental. O governo atual trouxe o país e a sua diplomacia de volta aos tempos da ditadura militar, que é muito apreciada pelo chefe de governo.

Isolado, Brasil perde credibilidade em cúpula ambiental de Estocolmo

Deutsche Welle

02/06/22 - 07h58

De protagonista na diplomacia climática a pária internacional, país aprofunda isolamento em reedição da histórica conferência de meio ambiente de 1972, na capital sueca.Cinco décadas após sediar a primeira reunião da história sobre meio ambiente e inserir o tema no mundo diplomático, Estocolmo volta a ser palco de discussões a partir desta quinta-feira (02/06), sob um clima mais sombrio.

Em 1972, a então Conferência das Nações Unidas sobre o Meio Ambiente Humano, o primeiro grande evento da ONU, trazia à tona as primeiras evidências de que o estilo de vida, principalmente dos países ricos, causava estragos de dimensões planetárias. A poluição, vista como um lado negativo da industrialização acelerada, era considerada o maior problema na época.

A reedição da conferência na capital da Suécia em 2022, batizada de Estocolmo+50, se situa num contexto mais desconfortável. Passados 50 anos, o diagnóstico atualizado da saúde do planeta vai muito além da poluição: mudanças climáticas e perda da biodiversidade e de espaços naturais entram na lista como ameaças graves ao bem-estar da humanidade.

Embora esteja sob a sombra da guerra na vizinha Ucrânia e todos os seus impactos, como a insegurança alimentar, num mundo que ainda tenta superar a pandemia de covid-19, a reunião tenta recuperar o espírito pioneiro de 1972 e busca um lugar na história do movimento ambiental.

Pelo menos dez chefes de Estado devem comparecer; Jair Bolsonaro não estará entre eles. O Brasil deverá ser representado pelo ministro do Meio Ambiente, Joaquim Leite, e a secretária de Amazônia e Serviços Ambientais, Marta Lisli Giannichi.

A expectativa de que a delegação brasileira cause qualquer boa impressão é baixa. “O Brasil do governo Bolsonaro é completamente obtuso em relação à importância ambiental, o que gera isolamento e consome o capital diplomático importante que o país tinha no plano internacional”, analisa Celso Lafer, ex-ministro das Relações Exteriores, em entrevista à DW.

Política do isolamento

O isolamento internacional parece ter sido opção do governo Bolsonaro quando o debate se volta para o meio ambiente. Em outras reuniões da ONU, como a Assembleia Geral de 2019, ele criticou o empenho de outros países em iniciativas que visam a preservação da Amazônia e a extensão de terras destinadas aos povos indígenas.

Naquele primeiro ano de seu mandato, Bolsonaro via sua imagem derreter junto à opinião pública à medida que a Amazônia sofria uma das mais severas temporadas de queimadas. A grande repercussão do desastre ambiental foi descrita como “ataques sensacionalistas” pelo presidente, que afirmou na plenária ter “um compromisso solene com a preservação do meio ambiente”.

Mas não é o que mostram os dados observados por satélite e divulgados anualmente há três décadas pelo sistema de monitoramento operado pelo Instituto Nacional de Pesquisas Espaciais (Inpe). Nos três primeiros anos da gestão Bolsonaro, a alta do desmatamento da maior floresta tropical foi de 52,9% em comparação com os anos anteriores.

“O Brasil perdeu credibilidade, está numa posição defensiva. Não é uma questão ideológica, é uma questão de número. Não tem como negar o aumento do desmatamento, estimulado tacitamente pelo governo, e o desrespeito aos direitos indígenas”, comenta Fábio Feldmann, ambientalista com longo histórico de atuação.

Nenhum porta-voz do governo federal respondeu aos pedidos de entrevista da DW Brasil.

Do protagonismo à pária

Meses antes da conferência em Estocolmo, publicações que apontavam o abismo para o qual caminhava a humanidade influenciavam a opinião pública e os rumos das conversas durante o evento.

Entre os exemplos estão o livro This endangered planet, de 1971, escrito por Richard Falk, e o relatório Limits to growth, de 1972, coordenado pelo Clube de Roma, que projetava que o crescimento econômico e populacional contínuo esgotaria os recursos da Terra e levaria ao colapso global até 2070.

Era o começo da compreensão da crise ambiental – que evoluiu bastante até os dias atuais, analisa Feldmann, amparada pela produção de conhecimento científico na área. “Em 1972 havia uma certa dificuldade dos países de entender a questão ambiental, era um tema novo, por isso houve naquela época essa linha de que tudo se tratava de uma conspiração”, argumenta.

Essa teoria, adiciona, não se sustenta em 2022, como tenta manter Bolsonaro. “É impossível negar a realidade hoje. O governo não controla mais toda a informação, a sociedade civil também monitora o desmatamento e os indicadores ambientais, e os cientistas comunicam bem à sociedade os dados que produz”, pontua.

O cenário atual parece aquele visto há 50 anos, quando o Brasil vivia uma ditadura militar, era alvo de críticas por violações dos direitos humanos e tinha péssimos indicadores ambientais e sociais. Ao mesmo tempo, chamava atenção pelas riquezas naturais, como a biodiversidade e reserva de água potável.

“A partir de Estocolmo, consolidou-se a percepção internacional de que o Brasil não parecia capaz de preservar esse extraordinário patrimônio. Isto se fortaleceu ainda mais nos anos subsequentes, agravando-se na segunda metade dos anos 80 em razão da repercussão da intensificação das queimadas na Amazônia”, escreve o diplomata André Aranha Corrêa do Lago, no livro Conferências de desenvolvimento sustentável.

Naquela ocasião, o posicionamento brasileiro foi visto como bastante atrasado, e chegou-se a falar que o país tentava boicotar a conferência. O Brasil tentava convencer outros países em desenvolvimento de que a reunião em Estocolmo era uma estratégia para impedir a industrialização das nações mais atrasadas – e mais pobres.

“O país não compreendeu a conferência, interpretou de maneira incorreta. Não conseguia entender que a crise ambiental havia chegado para ficar”, opina Feldmann.

O legado de Estocolmo

Mas tudo mudou depois da Rio 92 (Conferência das Nações Unidas sobre Meio Ambiente e Desenvolvimento), cujo processo de candidatura ocorreu quando o Brasil retornava ao regime democrático.

O empenho do país em sediar o evento se devia principalmente à deterioração de sua imagem no exterior, narra Corrêa do Lago em seu livro. Esse fato “vinha sendo acompanhado com preocupação pelo Itamaraty e, principalmente, por suas repartições na Europa e nos EUA, onde o Brasil se tornara o grande alvo de grupos ambientalistas e da imprensa”, diz um trecho.

Ministro à época, Celso Lafer afirma que o sucesso da Rio 92 consagrou o tema ambiental de grande peso na agenda internacional. “Ela foi a menos governamental das grandes conferências diplomáticas. Não teve nada de improvisação; muitos documentos foram preparados”, detalha.

Para Feldmann, um dado em particular ressalta a mobilização que o debate causou na capital fluminense: “Foram 102 chefes de Estado que compareceram ao Rio de Janeiro. Em Estocolmo, em 1972, foi apenas uma, a primeira-ministra da Índia, Indira Gandhi.”

Em resposta à desconfiança da primeira reunião na Suécia, o corpo diplomático brasileiro é apontado como o mais atuante para que o desenvolvimento dos países mais pobres não fosse impedido diante das questões ambientais. Nascia o conceito de desenvolvimento sustentável, que se firmou nas conferências seguintes da ONU.

“Diante da gravidade do problema, o copo parece muito vazio. Mas do ponto de vista do que se avançou desde então, está meio cheio”, classifica Lafer, mencionando entre os legados a criação de órgãos como o Programa das Nações Unidas para o Meio Ambiente (Pnuma) e o Painel Intergovernamental sobre Mudanças Climáticas (IPCC).

Apesar de as ações para frear a degradação ambiental em todo o planeta ainda estejam longe da efetividade necessária, Feldmann vê a reedição de Estocolmo como uma celebração. “Ainda precisamos de muito avanço, mas toda essa mobilização em torno da pauta ambiental só reforça o legado da conferência histórica de 1972”, opina.

https://www.istoedinheiro.com.br/isolado-brasil-perde-credibilidade-em-cupula-ambiental-de-estocolmo/

Meu mais recente livro – que não tem nada a ver com o governo atual ou com sua diplomacia esquizofrênica, já vou logo avisando – ficou final...