As projeções de alguns economistas sobre um Bretton Woods III são, como diria Mark Twain, altamente exageradas. O dólar parece destinado a servir de moeda internacional, para reservas nacionais, para os intercâmbios globais, durante muitos anos mais.

The US dollar might slip, but it will continue to rule

The international monetary system may be at the threshold of significant change from a combination of economic, geopolitical, and technological forces. But it is an open question whether these forces will knock the US dollar off its pedestal as the dominant international currency, which it has been for much of the post–World War II period. How these forces play out will have major ramifications for the evolution of the world order, because financial power is a key element of soft power.

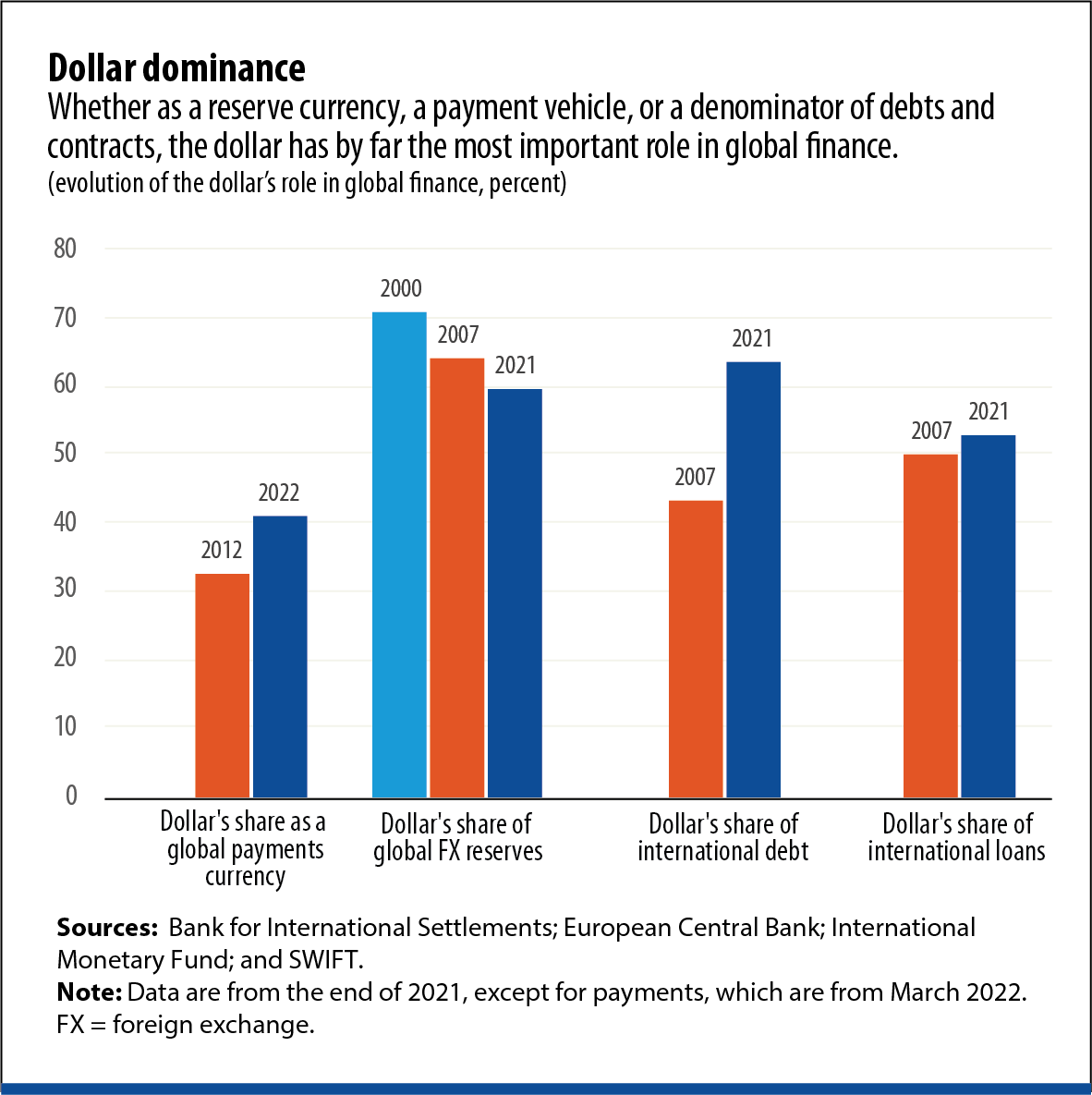

The dollar dominates every aspect of global finance. Nearly 60 percent of the world’s central banks' foreign exchange reserves, essentially their rainy-day funds, are invested in dollar-denominated assets. Almost all commodity contracts, including those for oil, are priced and settled in dollars. The dollar is used to denominate and settle a majority of international financial transactions (see chart).

The preeminence of the dollar gives the United States considerable power and influence. Because transactions entailing use of the dollar invariably involve the US banking system, the US government can severely punish countries, such as Iran and Russia, by imposing sanctions that limit their access to global finance. It also means that the fiscal and monetary policies of the US government affect the rest of the world because they influence the value of the dollar. And it allows the United States to punch well above its weight in global GDP and trade, which has long rankled US rivals and allies alike.

Changes afoot

Changes are underway that could undermine this supremacy.

Raw US economic dominance is shrinking. The US economy now accounts for about 25 percent of global GDP (at market exchange rates), down from 30 percent in 2000. Indeed, the locus of economic power, as measured by the share of global output and trade, has been shifting toward emerging market economies, led by China, for more than two decades.

The emergence of digital currencies, both private and official, is shaking up domestic and international finance. Consider international payments. They involve multiple currencies, payment systems operating on diverse protocols, and institutions governed by varying regulations. As a result, cross-border payments have tended to be slow, expensive, and difficult to track in real time. New technologies spawned by the cryptocurrency revolution now make for cheaper and practically instantaneous payment and settlement of transactions.

Even central banks are getting into the game, using the new technologies to increase the efficiency of payment and settlement mechanisms for cross-border transactions by their domestic financial institutions. The central banks of China, Hong Kong SAR, Thailand, and the United Arab Emirates are collaborating on one such effort, and other central bank consortia are engaged in similar exercises.

These developments will alleviate payment-related frictions in international trade, because quicker settlement reduces risks from exchange rate volatility. Exporters and importers will enjoy less need to hedge against the risks of exchange rate volatility that stem from long delays in processing and finalizing payments. Economic migrants sending remittances home, a key source of revenue for many developing economies, will also benefit from lower fees.

Changes are also afoot in foreign exchange markets. For example, transactions between pairs of emerging market currencies are becoming easier as financial markets and payment systems mature. Typically, converting such currencies to dollars, and vice versa, has been easier and cheaper than exchanging them for one another. But China and India, for example, will soon no longer need to exchange their respective currencies for dollars to conduct trade cheaply. Rather, exchanging renminbi for rupees directly will become cheaper. Consequently, the reliance on “vehicle currencies,” particularly the dollar, will decline.

In short, as international payments become easier and perhaps even increase in volume as frictions recede, the role of the dollar in intermediating such payments could decline. In tandem with these changes, the dollar’s primacy in the denomination of various transactions will decline. Pricing of oil contracts in dollars is less important, for example, if China can use renminbi to pay for its oil purchases from Russia or Saudi Arabia.

Digital currencies

Digital technologies affect other aspects of money. With the rapid decline in the use of cash, many central banks are moving forward—or at least experimenting—with central bank digital currencies (CBDCs). China, among major economies, is well into advanced trials of its CBDC.

The prospect of a digital renminbi available worldwide has intensified speculation that China’s currency could gain in prominence and perhaps even rival the dollar. But a digital renminbi by itself will not shift the balance of power among major currencies. After all, most international payments are already digital. Rather, it is China’s Cross-Border Interbank System (CIPS), which can communicate directly with other countries’ payment systems, that will enhance the renminbi’s role as an international payment currency.

Even so, the renminbi still lacks some key attributes that reserve currencies typically need to be considered reliable stores of value. China has made some progress in this area—removing restrictions on cross-border capital flows, leaving its currency’s value to market forces, and broadening foreign investors’ access to its bond markets. But the government has rejected institutional changes essential to garnering the trust of foreign investors, including an independent central bank and the rule of law. Indeed, China is alone among reserve currency economies in not sharing these characteristics.

Still, the renminbi has made some progress as an international currency. By some measures, it is used for about 3 percent of international payment transactions, and about 3 percent of global foreign exchange reserves are held in renminbi. Such measures of renminbi prominence will almost certainly increase as the Chinese economy and its financial markets grow and foreign investors, including central banks, allocate a greater portion of their portfolios to renminbi-denominated assets—if for no reason other than diversification. But it is unlikely that the renminbi will pose a serious threat to the dollar’s dominance unless the Chinese government embraces both market-oriented economic reforms and upgrades to its institutional framework.

A mixed blessing

The new technologies will both help and hinder emerging market economies, with collateral effects that—coupled with other developments—in the end may enhance dollar dominance rather than erode it.

On one hand, as mentioned earlier, new financial technologies will improve access to global financial markets for firms and households in emerging market and developing economies. Reduced frictions in international payments will enable these economies’ firms to gain access to global pools of capital and give their households easier access to opportunities for international portfolio diversification—permitting better returns on their savings while managing risk.

On the other hand, the proliferation of conduits for money to flow across national borders will intensify developing economies’ vulnerability to the vagaries of major central banks’ policies and the whims of domestic and international investors. It is also likely to render capital controls less effective. Even cryptocurrencies such as Bitcoin have been channels for capital flight when a country’s currency is collapsing and domestic investors lose faith in their country’s banking system. In short, greater capital flow and exchange rate volatility will further complicate domestic policy management, with deleterious consequences for economic and financial stability in these economies.

The natural response of policymakers in emerging markets is to protect their economies against such outcomes by further expanding their stocks of hard currency foreign exchange reserves. But Russia’s loss of access to the bulk of its foreign exchange reserves—the result of Western sanctions imposed in response to its invasion of Ukraine—shows that such buffers might be unavailable in times of dire need. This has generated speculation that emerging market economies will look to other reserve assets—such as gold, cryptocurrencies, or the renminbi—as alternatives to government bonds issued by advanced economies.

The reality, though, is that assets such as gold are not viable alternatives because their markets are not liquid enough; it would be difficult to sell a large stock of gold within a short period without setting off a plunge in gold prices. Cryptocurrencies such as Bitcoin have the additional problem of being highly unstable in value. Even renminbi reserves might be of limited help because that currency is not fully convertible.

For the foreseeable future, there is likely to be strong and perhaps even rising demand for “safe assets” that are liquid, available in large quantities, and backed by countries with trusted financial systems. There are limited supplies of such assets, and the US dollar—which represents a powerful combination of the world’s largest economy and financial system, backed by a strong institutional framework—remains the dominant supplier. The desire for diversification has led to recent modest increases in the shares of Australian, Canadian, and New Zealand dollars in global foreign exchange reserves, but these—and other leading reserve currencies, such as the euro, the British pound, and the Japanese yen—have only marginally dented the US dollar’s share.

Innocent bystanders

Changes coming to the international monetary system pose additional threats to the currencies of smaller and less developed economies. Some of these countries—especially those with central banks or currencies that lack credibility—could be overrun by nonnative digital currencies.

It is possible that national currencies issued by their central banks, particularly currencies seen as less convenient to use or volatile in value, could be displaced by stablecoins—private cryptocurrencies issued by multinational corporations or global banks and usually backed by US dollars to maintain stability—or by CBDCs issued by major economies. Even a volatile cryptocurrency such as Bitcoin might, in addition to enabling capital flight, be preferred to the local currency during economic turmoil.

But it is more likely that economic turmoil would result in further dollarization of economies, particularly if digital versions of such well-known currencies as the dollar become easily available worldwide.

Although digital technologies enable new forms of money that could challenge fiat currencies and set off a new era of domestic and international currency competition, it is equally likely that these new forces will create more centralization, with some currencies accreting even more power and influence. In other words, many of these changes might reinforce rather than weaken the dollar’s dominance.

The dollar trap

There are other forces that sustain the dollar’s dominance, especially the prospect of losses were the dollar to falter. Foreign investors, including central banks, hold nearly $8 trillion in US government debt. Overall US financial obligations to the rest of the world total $53 trillion. Because these liabilities are denominated in dollars, a plunge in the value of the dollar would make no difference to the amount the United States owes but would reduce the value of those assets in terms of the currencies of the countries that own them. China’s holdings of US government bonds, for instance, would be worth less in renminbi.

On the flip side, US investors’ holdings of foreign assets, about $35 trillion, are denominated almost entirely in foreign currencies. Hence, an increase in the value of those currencies relative to the dollar would mean that they are worth more when converted into dollars. Thus, although the United States is a net debtor to the rest of the world, a fall in the value of its currency would result in a windfall to the United States and a big loss to the rest of the world. For the foreseeable future, then, even dollar detractors might fear a sharp fall in its value, leaving the world stuck in a “dollar trap.”

The upshot is that the dollar’s role as the dominant reserve currency will likely persist, even if its status as a payment currency erodes, which itself is uncertain.

A likelier prospect is a reshuffling of the relative importance of other currencies while the dollar retains its primacy. Rather than knocking the dollar off its pedestal, new technologies and geopolitical developments might entrench its position.

ESWAR PRASAD is a professor at Cornell University and a senior fellow at the Brookings Institution.