Temas de relações internacionais, de política externa e de diplomacia brasileira, com ênfase em políticas econômicas, viagens, livros e cultura em geral. Um quilombo de resistência intelectual em defesa da racionalidade, da inteligência e das liberdades democráticas. Ver também minha página: www.pralmeida.net (em construção).

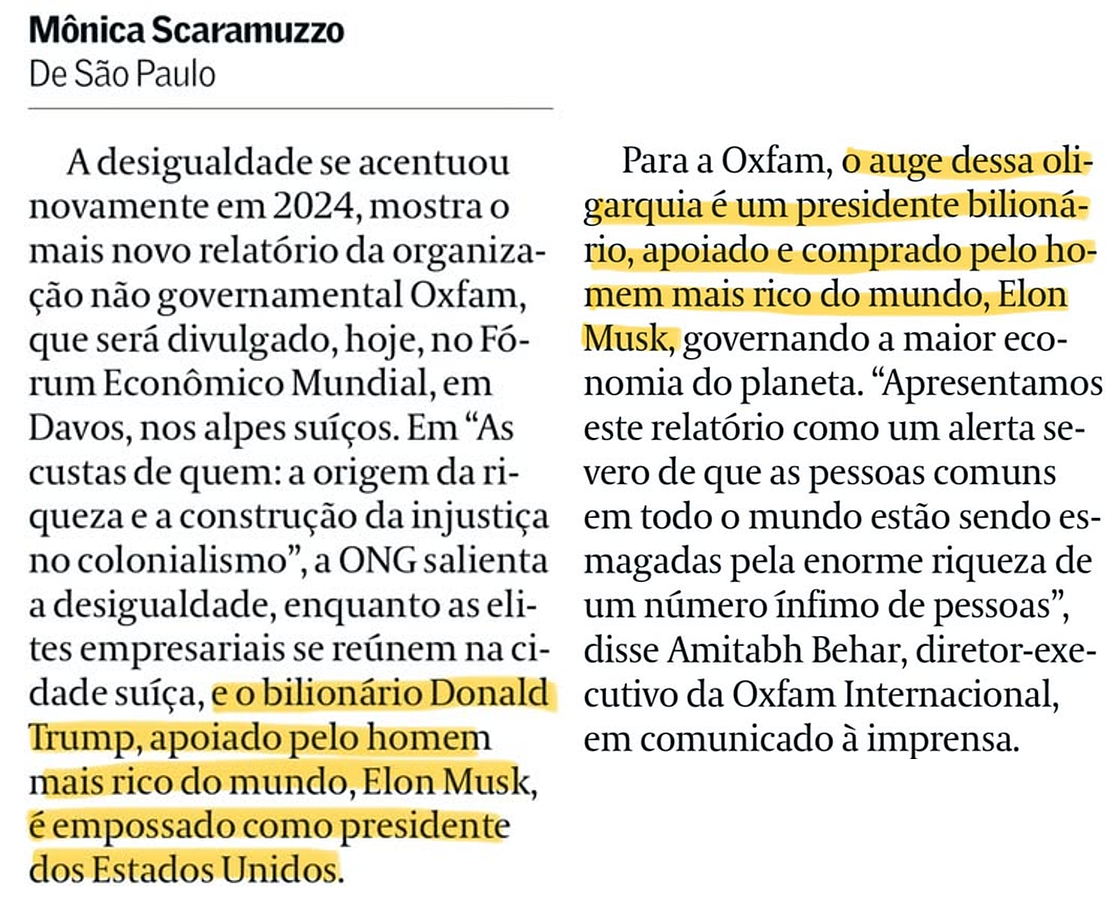

A Oxfam, aquela ONG britânica que existe para nos lembrar que o capitalismo é um sistema econômico tão perverso que só pode ter sido inventado pelo tinhoso em pessoa, divulgou hoje, em Davos, o seu já tradicional relatório sobre a desigualdade global. Segundo o relatório, a soma dos patrimônios dos bilionários soma, agora, US$ 15 trilhões, contra US$ 13 trilhões há apenas um ano, o crescimento mais rápido da história. Isso fez com que a ONG previsse a existência de nada menos que 5 trilionários daqui a 10 anos. Só não fiquei mais alarmado do que quando leio relatórios sobre o aquecimento global. Aliás, está aí um estudo interessante, a correlação entre o número de bilionários e a temperatura do planeta. Perdão, divago.

A divulgação do relatório, coincidentemente ou não, se dá no dia da posse de Donald Trump. Esta coincidência é lembrada em dois trechos da reportagem. Em ambos, menciona-se o bilionário Trump e seu fiel escudeiro, o homem mais rico do mundo, Elon Musk, como símbolos dessa criminosa concentração de renda. Os Estados Unidos estariam agora liderando o que de pior o capitalismo produziu ao longo dos séculos.

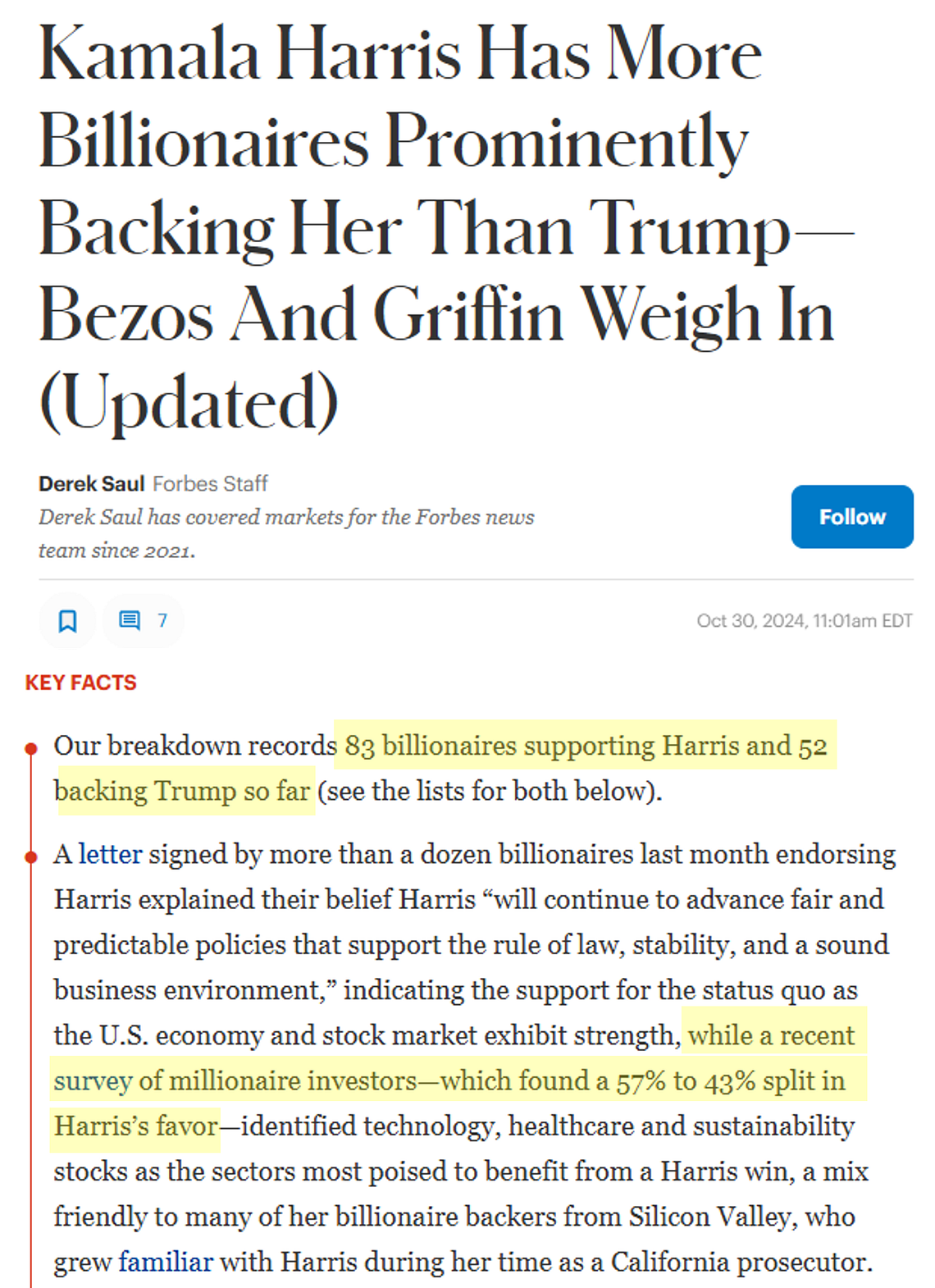

Só tem um probleminha com esse simbolismo: segundo levantamento da Forbes, 83 bilionários apoiaram Kamala Harris, contra 52 que apoiaram Trump. E entre os apenas milionários, 57% apoiaram Kamala, contra 43% que apoiaram Trump.

Segundo a revista, os bilionários viam na democrata alguém que “daria continuidade a políticas previsíveis que apoiariam o império da lei, a estabilidade e um ambiente de negócios saudável”. Ou seja, os bilionários consideravam Harris como a mais indicada para manter um ambiente em que… as suas fortunas cresceriam ainda mais! Aliás, não custa lembrar que em 2024, ano em que os bilionários amealharam US$ 2 trilhões adicionais, o presidente era ainda Joe Biden.

Ok, alguns bilionários devem ter votado em Kamala para aliviar um pouco o seu peso de consciência por serem bilionários. Mas não tenho dúvida de que a maioria estava fazendo uma conta de vantagens/desvantagens em relação aos seus próprios interesses. Assim, Trump pode até servir como uma caricatura da concentração de renda, mas quem votou nele foi a classe média baixa, não os bilionários.

A Oxfam, como toda organização de esquerda, acha que fala em nome dos pobres. Isso sim, é só uma caricatura.

Blog do Marcelo Guterman é uma publicação apoiada pelos leitores.

Roberto Macedo - Distribuição de riqueza é mais concentrada

O Estado de S. Paulo

As desigualdades de renda e de riqueza no Brasil remontam ao período colonial do País, e não há solução à vista

É sabido que há mais estudos sobre a distribuição de renda do que a distribuição de riqueza, em que a disponibilidade de dados é menor e mais difícil de organizar, em particular se envolve também outros países. Um novo e bem-vindo estudo sobre a mesma, realizado no exterior pelo Union Bank of Switzerland (UBS), foi objeto de reportagem no jornal Valor Econômico de 11/7/2024. Constatou que aqui houve aumento da concentração da riqueza e adicionou outras considerações, inclusive sobre o índice de concentração de Gini, que abordarei mais à frente neste texto.

Segundo esse novo estudo, digno de maior atenção, realizado como parte de um relatório desse banco sobre a riqueza mundial, noBrasil a “concentração de riqueza aumentou 16,8% nos últimos 15 anos e o País já ocupa o terceiro lugar no ranking de desigualdade entre 56 nações, atrás apenas de Rússia e África do Sul”. É interessante ver também a Rússia nessa lista, pois depois de décadas de um regime dito comunista acabou desembocando numa situação desse tipo.

O estudo, que abrangeu o expressivo número de 36 países, também aponta que enquanto entre “2000 a 2010 houve uma expansão de riqueza no Brasil de 384%, com uma média anual de 15%, nos 13 anos seguintes (acrescento, entre 2011 a 2023) a taxa caiu para 55%, com um ritmo anual de apenas 3%”. Outro aspecto interessante é que o estudo prevê que “até 2028 o Brasil terá 83 mil novos milionários, em um total de 463.797 indivíduos, (...) com patrimônio igual ou superior a US$ 1 milhão”. Tanto na renda como na riqueza o Brasil sai mal na foto da distribuição. O UBS aponta que o menor crescimento da riqueza no segundo e mais recente período citado veio de fatores como a depreciação da sua moeda, inflação, queda da produtividade e menor crescimento econômico. Outro dado interessante é que “14 indivíduos no mundo contam cada um com fortunas de mais de US$ 100 bilhões. Esse grupo, no total, concentra US$ 2 trilhões em riqueza”.

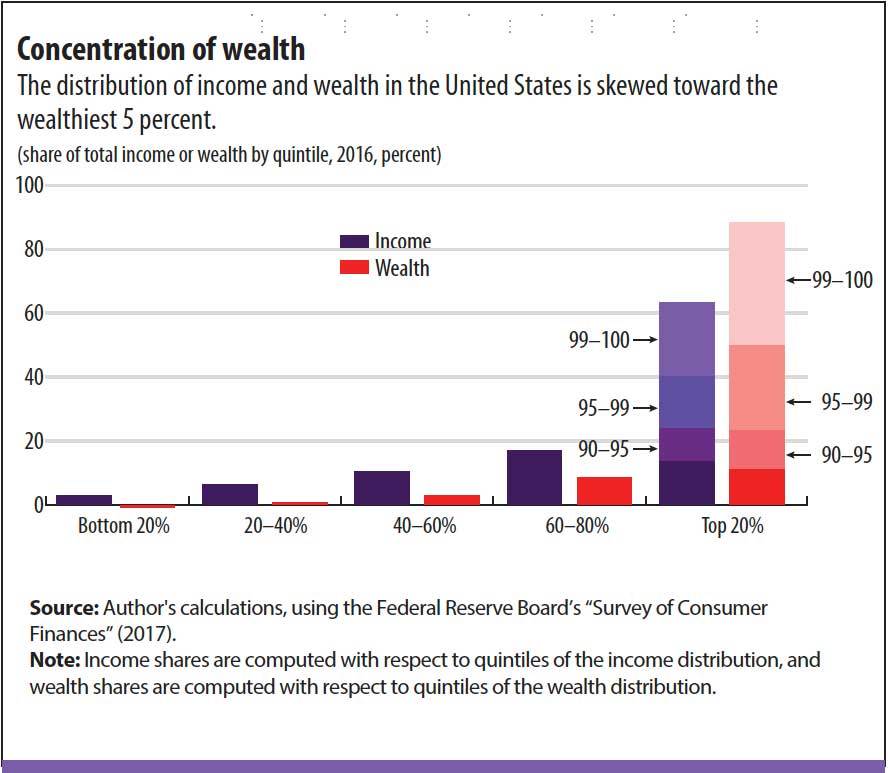

O estudo também utiliza o índice de concentração de Gini para examinar o grau de concentração dentro de cada país. Esse índice varia entre 0 e 1, que indica menor e maior concentração, respectivamente, e no Brasil ele passou de 0,7 para 0,81 nos últimos 15 anos, revelando outro aspecto do aumento da concentração de riqueza. Quanto ao índice de Gini da distribuição de renda, um estudo da Fundação Getulio Vargas, usando dados da Pesquisa Nacional por Amostra de Domicílios Contínua (Pnad Contínua) e da Receita Federal, mostrou que o índice chegou a 0,7068 em 2020, valor é superior ao 0,6013 calculado apenas pela Pnad Contínua. Em qualquer caso, são valores inferiores ao último dado do UBS (0,81). Ou seja, a concentração de patrimônio é superior à da renda.

As desigualdades de renda e de riqueza no Brasil remontam ao período colonial do País, marcado inclusive pela escravidão. Os mais pobres têm maior crescimento populacional e são menos educados nos seus lares, nas escolas, no trabalho e no seu meio social. Além disso sua oferta no mercado de trabalho é maior relativamente à demanda do que os demais grupos sociais. Com tudo isso, têm menor renda, sendo-lhes muito difícil acumular patrimônio.

Esse quadro foi se formando há séculos e não tem solução imediata. Uma das razões é que as lideranças políticas não revelam uma efetiva preocupação com ele, com o que são escassas as medidas que podem modificá-lo com profundidade. Algo que poderia ajudar seria uma forte aceleração do crescimento econômico, mas, no governo federal, o Congresso, constituído predominantemente por cidadãos de maior renda, não pauta seriamente esse assunto, estando mais preocupado em atender a seus interesses pessoais e de grupos politicamente atuantes em busca de vantagens. O presidente atua de modo populista, procurando ganhos eleitorais com distribuição de benefícios sociais que trazem pouco alívio a essa situação e causam prejuízo ao crescimento econômico, pois reduzem a taxa de investimento público. Os mais pobres tampouco têm atuação política para mudar essa situação, atuando apenas como eleitores que caem nas mãos de políticos populistas.

O baixo crescimento do Brasil é uma praga que nos assalta há mais de 40 anos, e a sociedade e até mesmo analistas econômicos parecem se conformar com isso, dizendo que o crescimento potencial da economia é de apenas 2% ao ano e incorporando essa previsão para os anos vindouros. Falta um sério plano de governo para o País sair desse conformismo com a mediocridade desse crescimento. Eu estava cursando o ensino superior num período em que a economia chegou a crescer a uma média anual de 7%, o que me trouxe grandes oportunidades em termos de educação e trabalho.

Mas hoje não há solução à vista ou mesmo algo mais distante no horizonte para esse quadro. Quando o denuncio, como neste artigo, isso apazigua um pouco a minha consciência, o que dura pouco, pois logo depois voltam as minhas preocupações com esse impasse que vem prejudicando o País e os brasileiros.

Tomorrow here in Washington is the inauguration of Joe Biden as the 46th president of the United States. Among the many crises on his plate, inequality is perhaps the most pervasive. Heather Boushey, an incoming member of President-elect Biden's White House Council on Economic Advisors, carved out a blueprint to address this very issue in our latest edition of F&D.

She writes that workers and their families on the wrong side of the many US economic disparities are there for several reasons—including a stubborn reliance by policymakers on markets to do the work of government, and the racism and sexism, sometimes written into law, that blind policymakers to injustice and to economic sense.

The COVID-19 pandemic is shining an unforgiving spotlight on the many inequalities in the United States, demonstrating how pervasive they are and that they put the nation at risk for other systemic shocks. To stop the spread of the virus and emerge from a crushing recession, these fundamental inequalities must be addressed. Otherwise not only is a slow economic recovery more than likely, but the odds grow that the next shock—health or otherwise—will again throw millions out of work and subject their families to fear, hunger, and lasting economic scars.

Before the pandemic, the United States was in the midst of a decade-long recovery from the Great Recession, which began in December 2007. But not all Americans experienced that recovery in the same way. The top 1 percent emerged as strong as ever in terms of wealth, regaining what they had lost by 2012. As of March 2020, however, US working- and middle-class families had barely recovered their lost wealth, and many families, especially those of color, never recovered. Even amid a strong recovery, the United States was burdened by extraordinary economic and racial inequality.

Today, stark differences among US workers and their families make the current recovery neither U- nor V-shaped but rather one that resembles a sideways Y, with those benefiting from a stock market recovery or employed standing on the branch of the Y that points up unaffected by the recession, and those on the bottom branch facing perhaps years of struggle. And there are stark differences of race and class between the upper and lower legs of that sideways Y. This recession provides an opportunity for policymakers to address these inequalities with transformative policy changes to produce a healthier and more resilient economy that delivers strong, stable, and broad-based growth and prosperity.

Disparities abound

Workers and their families on the wrong side of the many US economic disparities are there for several reasons—including a stubborn reliance by policymakers on markets to do the work of government and the racism and sexism, sometimes written into law, that blind policymakers to injustice and to economic sense.

This article will identify specific causes of economic inequality in the United States and then explain how to address them.

Markets: Beginning in the 1980s, conservative economists began to make the case that unfettered markets were the only way to deliver sustained growth and well-being. This ideology, with modest exceptions, has governed US economic policymaking ever since. But it has not delivered. Moreover, the supposedly neutral and fair rules that govern markets have in fact shifted economic risk away from corporations and the wealthy toward medium- and low-income families. This has never been more apparent than now, when the coronavirus has caused mostly low-income workers to either lose their jobs or have to work in employment that exposes them to the risk of contracting and spreading the disease.

Tax cuts, weak public investment: President Donald Trump’s 2017 tax cut, which benefited largely the better-off, is only the most recent manifestation of a tax-cutting philosophy that has governed US fiscal policy for decades. These measures have starved the nation of resources that could be used to fund basic governmental functions and critical public investments. As a result, public investment as a share of GDP—the value of goods and services produced in the United States in a year—has fallen to its lowest level since 1947.

Eroding worker power: The ability of US workers to bargain for higher wages and benefits and better and safer working conditions has been sapped by years of anti-union court and administrative rulings. And in 27 states, right-to-work laws make it harder for unions to form. As employers gained the upper hand, wages stagnated, and worker safety has suffered, especially during the pandemic.

Economic concentration: US antitrust policy and enforcement have allowed industries across the United States to become increasingly concentrated, giving large businesses market power to set prices, eliminate competitors, suppress wages, and hobble innovation. What’s more, there is evidence that this is dampening firms’ investment. Some are thriving in the midst of—indeed because of—the pandemic, while small businesses struggle to survive.

Measuring the economy: Before the 1980s, when US economic inequality began its upward trajectory, growth in GDP was a reasonably reliable indicator of the well-being of most Americans. But as economic inequality has risen close to its 1920 levels, the benefits of GDP growth have gone disproportionately to the top 10 percent of earners, while income growth for the vast majority of people has been slower than that of GDP—in some cases, none at all. For that reason, GDP reflects mostly how the better-off are doing. As GDP recovers in the coming months, therefore, it will give policymakers false signals about whether average Americans are recovering.

Racism and sexism: The disparate health and economic consequences of the coronavirus recession reinforce the reality and history of racism and sexism in the United States. The median earnings for a Black household are 59 percent of those of a White household, and for men and women of all races, a median woman earns 81 cents for every dollar earned by a man. The results of job segregation are apparent, with health care and service workers on the pandemic front lines. Despite being essential, some of these jobs—in which women and minorities are overrepresented—are the least likely to have benefits such as paid sick time or employer-provided health insurance.

These problems are largely the result of decades of failed policies supported more by ideology than evidence. A distorted economic narrative that lionizes markets has led to the weakening of public institutions and the acceptability of less funding for democratic institutions of governance, greater economic concentration, reduced worker power, and the discriminatory effect of laissez-faire labor rules. The role of policy choices in arranging the market structure is unmistakable and enduring.

Building a strong, equitable economy

Transforming the US economy requires policymakers to recognize that markets cannot perform the work of government.

The first step is to eradicate COVID-19. It has to be the first priority, not only for public health but also for the US economy. Beyond that, encouraging a strong and sustained recovery that delivers broadly shared growth also requires the United States to address its long-term problems: a costly health system that leaves millions with insufficient care, an education system designed not to end inequality but to preserve it, lack of basic economic stability for most families, and climate change.

Major public investments are required to deal with each issue. While it is not necessary to worry now about paying for them, the nation should put in place significant tax increases, primarily or entirely on the wealthy, to begin investing in these long-term solutions. The country should tax the enormous wealth concentrated at the top that is being saved, or kept overseas, and not being invested in the economy or in solving societal problems.

Policymakers also must address the economic concentration that has created monopsony power (a single or handful of buyers or employers) that keeps wages down and threatens small businesses, which are the lifeblood of innovation and economic dynamism. The first step is to ensure that the recession and the programs designed to help businesses survive the crisis don’t exacerbate this trend. Thus far, federal policies to address the economic downturn have provided far greater aid to large businesses than to small ones.

Policymakers also must ensure that federal government funds are directed to productive uses that support workers and customers, and not to rewarding wealthy shareholders. Corporations receiving aid should be barred from issuing dividends and carrying out stock buybacks, and banks should be required to suspend capital distributions during the crisis to support lending to the real economy.

Even more fundamental to addressing excessive concentration is strengthening US antitrust enforcement, which is weaker than it has been in decades. The antitrust laws themselves also need to be bolstered, particularly with respect to the rules governing mergers and exclusionary conduct. Legislators should consider creating a digital regulatory authority to enforce privacy laws and enhance competition in digital markets.

The country also needs to better understand who benefits, or does not, from recovery policies and what further actions are needed. Because overall GDP is not up to that task, income must be disaggregated at all levels to measure progress or lack thereof for all groups—which would enable the United States to lay the groundwork for understanding what other actions are needed to ensure more people benefit from the recovery.

US economic inequality is firmly tied to the issue of racial inequality. The unmistakable message of the Black Lives Matter movement is that Americans of color never have been able to trust government to act on their behalf. Government must work to ensure that low-income Black, Latinx, and Native American people can both develop and deploy their talents and skills in the economy.

Taxing wealth, which is disproportionately owned by White Americans, is one solution. But for that to address racial inequities adequately, the proceeds of the wealth tax must benefit the majority of the nonwealthy. The proceeds must be directed to the most urgently needed investments, such as in COVID-19 testing and treatment in communities of color, in policies that expressly and progressively support low-wage workers and care workers, and in engagement with minority-owned small businesses. Otherwise, pervasive inequities will be further entrenched.

A significant reason for the gender earnings gap is the lack of a national paid family and medical leave policy and the absence of a national program to ensure that families have access to quality, affordable childcare and prekindergarten education. Families with children that do not have access to paid leave and childcare—or cannot afford them—have little choice but to put careers on hold. This happens to women far more often than to men. Legislation has been introduced in Congress to accomplish both of these goals, and these measures should get serious consideration in the next Congress.

Reason for optimism

There is reason to believe that the United States can enact policies to transform its economy and society. Until recently, some of the conversations taking place among policymakers and around dinner tables—inspired by COVID-19, the deep recession, the Black Lives Matter movement, and the recent presidential election—would have been relegated to the edges of public debate. Today that is not the case.

Yet the US political system is beset by deep partisanship and a constitutional and electoral system that makes it far easier to block transformative policies than enact them. But I am an optimist, and I still believe that the country could be at an inflection point, with the advantage going to those who develop and advocate progressive policies to reduce inequality and build an economy that produces strong, stable, and broad-based growth.

###

As always, if you have any comments or feedback about this article, or if you have ideas about future contributors and topics to explore, please do write me a note directly. I would love to hear from you.

PHOTOGRAPHER: CAYCE CLIFFORD FOR BLOOMBERG BUSINESSWEEK

Gabriel Zucman started his first real job the Monday after the collapse of Lehman Brothers. Fresh from the Paris School of Economics, where he’d studied with a professor named Thomas Piketty, Zucman had lined up an internship atExane, the French brokerage firm. He joined a team writing commentary for clients and was given a task that felt absurd: Explain the shattering of the global economy. “Nobody knew what was going on,” he recalls.

At that moment, Zucman was also pondering whether to pursue a doctorate. He was already skeptical of mainstream economics. Now the dismal science looked more than ever like a batch of elaborate theories that had no relevance outside academia. But one day, as the crisis rolled on, he encountered data showing billions of dollars moving into and out of big economies and smaller ones such as Bermuda, the Cayman Islands, Hong Kong, and Singapore. He’d never seen studies of these flows before. “Surely if I spend enough time I can understand what the story behind it is,” he remembers thinking. “We economists can be a little bit useful.”

A decade later, Zucman, 32, is an assistant professor at the University of California at Berkeley and theworld’s foremost expert on where the wealthy hide their money. His doctoral thesis, advised by Piketty, exposed trillions of dollars’ worth of tax evasion by the global rich. For his most influential work, he teamed up with his Berkeley colleague Emmanuel Saez, a fellow Frenchman and Piketty collaborator. Their 2016 paper, “Wealth Inequality in the United States Since 1913,” distilled a century of data to answer one of modern capitalism’s murkiest mysteries: How rich are the rich in the world’s wealthiest nation? The answer—far richer than previously imagined—thrust the pair deep into the American debate over inequality. Their data became the heart of Vermont Senator Bernie Sanders’s stump speech, recited to the outrage of his supporters during the 2016 Democratic presidential primary.

Zucman and Saez’s latest estimates show that the top 0.1% of taxpayers—about 170,000 families in a country of 330 million people—control 20% of American wealth, the highest share since 1929. The top 1% control 39% of U.S. wealth, and the bottom 90% have only 26%. The bottom half of Americans combined have a negative net worth. The shift in wealth concentration over time charts as a U, dropping rapidly through the Great Depression and World War II, staying low through the 1960s and ’70s, and surging after the ’80s as middle-class wealth rolled in the opposite direction. Zucman has alsofoundthat multinational corporations move 40% of their foreign profits, about $600 billion a year, out of the countries where their money was made and into lower-tax jurisdictions.

Share of U.S. Wealth Held by the Top 1%

Data: Gabriel Zucman

Like many economists, Zucman and Saez have embraced the political implications of their research. Unlike many, they champion policy recommendations that are bold and aggressive. Before Massachusetts Senator Elizabeth Warren started her 2020 presidential campaign by proposing a wealth tax, she consulted the pair, whoestimatedthat her tax would bring in $2.8 trillion over the next decade. She conferred with them again before floating a corporate tax on profits above $100 million, which theycalculatedwould raise more than $1 trillion over 10 years. Sanders came looking for their advice on his estate tax plan, which would establish rates as high as 77% on billionaires. And when New York Representative Alexandria Ocasio-Cortez proposed on60 Minutesto hike the top marginal tax rate to as much as 70% on income above $10 million, Zucman and Saez were fast out with aNew York Timesop-edin support.

The pair has now written a cookbook of sorts for any 2020 candidate looking to soak the rich.The Triumph of Injustice, to be published by W.W. Norton & Co. early next year, focuses on how wealth disparity can be fought with tax policy. The tools Zucman has identified to date challenge a series of assumptions, fiercely held by many economists and policymakers, about how the world works: That unfettered globalization is a win-win proposition. That low taxes stimulate growth. That billionaires, and the superprofitable companies they found, are proof capitalism works. For Zucman, the evidence suggests otherwise. And without taking action, he argues, we risk an economic and political backlash far more destabilizing than the financial crisis that sparked his work.

The Wealth Detective

The Wealth Detective

America’s top wealth detective probes the secrets of the super rich in a tidy, white-walled office with an enviable view of the San Francisco Bay. His methods are unusually brute-force compared with those of recent-vintage U.S. economists, relying not on powerful computers, regression analyses, or predictive models, but on simple, voluminous spreadsheets compiling the tax tables, macroeconomic datasets, and cross-border-flow calculations of central banks. He does it on his own, only rarely outsourcing to graduate students.

“You can conduct this detective work only if you do it to a large extent yourself,” he says. “The wealth is not visible in plain sight—it’s visible in the data.” Lately, he adds, the Bay Area humming outside his window, “I see more of Silicon Valley in my Excel spreadsheets, especially in the amount of profits booked in Bermuda and Ireland.”

Zucman met his future wife, Claire Montialoux, in 2006, in a university economics class. She’s now finishing her Ph.D. dissertation, whichshowshow the U.S.’s expansion of the minimum wage in the late 1960s and ’70s helped black workers, narrowing the racial earnings gap. “We share the same vision for why we are doing social sciences,” Zucman says. “The ultimate goal is how can we do better?”

Born and raised in Paris, Zucman is the son of two doctors. His mother researches immunology, and his father treats HIV patients. Politics was a frequent dinnertime topic. He says the “traumatic political event of my youth” occurred when he was 15. Jean-Marie Le Pen, founder of the far-right National Front party, edged out a socialist candidate to win a spot in the final round of 2002 presidential voting. Zucman remembers joining the spontaneous protests that followed. “A lot of my political thinking since then has been focused on how we can avoid this disaster from happening again,” he says. “So far, we’ve failed.” (Le Pen’s daughter made the presidential runoff in 2017 and won almost twice as many votes as her father.)

His own graduate work in Paris saw him compile evidence that the world’s rich were stowing at least $7.6 trillion in offshore accounts, accounting for 8% of global household financial wealth; 80% of those assets were hidden from governments, resulting in about $200 billion in lost tax revenue per year. At the same time, he was helping his adviser, Piketty, pull together more than 300 years of wealth and incomedatafrom France, Germany, the U.K., and the U.S. They co-authored a paper on the numbers, which became a key part of Piketty’s surprise 2014bestseller,Capital in the Twenty-First Century. The following year, Zucman’s doctoral research was also published as a book,The Hidden Wealth of Nations.

He arrived in the U.S. in 2013, the same year President Obama was declaring inequality “the defining challenge of our time.” Zucman had been recruited to Berkeley by Saez, winner of economics’ prestigious John Bates Clark Medal in 2009 and aMacArthur Fellowshipin 2010. They took up offices next to each other and set about trying to solve the riddle of America’s hidden wealth, unveiling their estimates as a draft paper the following year.

None of it was easy. Tax collectors such as the IRS generally require taxpayers to report income, not wealth. And much of the world’s wealth is held in forms—homes, art, retirement accounts, non-dividend-paying stocks—that produce no income prior to a sale. A real estate mogul with a billion-dollar property portfolio and billions more in cash stashed overseas can still report a tiny income. Most inequality researchers therefore rely on voluntary surveys, which often fail to identify enough of the very richest, or data on the estate tax, which has gotten easier and easier to avoid.

Zucman and Saez started with the IRS. The agency opens its doors to researchers under strict conditions, and only Saez, a U.S. citizen, was allowed inside a facility, where he downloaded anonymized statistics up to the extreme end of the income scale. The duo then translated the data into wealth estimates. Saez had had the idea for a while. “I was doubting how that could actually be done, because there are so many complications,” he says. “And then Gabriel came along.” With each asset class, from equities and real estate to pensions and insurance, they painstakingly estimated the relationship between income and wealth in the U.S., checking and tweaking based on data from external sources.

They found that something cataclysmic happened around 1980. As Ronald Reagan was winning the White House, the top 0.1% controlled 7% of the nation’s wealth. By 2014, after a few decades of booming markets and stagnant wages, the top 0.1% had tripled its share, to 22%, a bit more wealth than the bottom 85% of the country controlled. The data showed the extent of the problem and the absence of a solution: In the aftermath of the financial crisis, while middle-class Americans were burdened by job losses and debt, the rich had swiftly resumed their party. Wealth that had vanished from financial markets after Lehman’s collapse had reappeared, doubling and tripling the portfolios of well-off investors.

U.S. Wealth Distribution, 2014

Data: World Inequality Database

Some eminent economists, including the University of Chicago’s Amir Sufi and Nobel laureate andNew York Timescolumnist Paul Krugman,endorsedthefindings, but others were skeptical. The new numbers were much higher than previous estimates, including those of the Federal Reserve’s Survey of Consumer Finances, which is based on detailed responses provided by Americans and is widely considered the best measure of U.S. wealth.

The disputes over Saez and Zucman’s methodology were highly technical. Fed economists said the Berkeley pair were underestimating the investment returns the very rich were earning, which had the counterintuitive effect of overestimating the fortunes from which they drew their income. Saez and Zucman rejected that criticism but made other adjustments to their method and updated the numbers to reflect revised macroeconomic data. Their estimate of the 0.1%’s wealth share dropped a couple of percentage points, to about 20%, still a startling figure. Then, in 2017, the Fed released a survey incorporating methods it said better captured the wealth of the very rich; the central bank cited Zucman and Saez’s work in an accompanying paper. Its latest figures showed a jump in inequality, with the top 1%’s share rising from 36% in 2013 to 39% in 2016, matching the pair’s estimate.

At conferences and seminars, Zucman’s peers still occasionally sound baffled by his work. Economists often aim for precise, unassailable conclusions, but he’s “comfortable getting a ‘rough justice’ answer to a question” if it helps fill in a big gap in knowledge, says Reed College economics professor Kimberly Clausing, an expert on corporate profit shifting. “I admire the fact that he’s willing to look at these harder questions.” Saez says Zucman’s “defining characteristic is that he’s not moored to the traditional economic model.” In the end, Saez adds, “that gives him tremendous power to make progress.”

Economists argue over the timing and size of the U.S.’s inequality surge, but few deny the broader trend. We live in an age in which the richest man in modern history is reduced by divorce to merely the richest man alive and in which even the most generous billionairescan’t give awaymoney faster than they’re bringing it in. The debate now raging is over how inequality deepened to this extent and what, if anything, to do about it.

On one hand are those who argue that great wealth is somehow natural, the result of technology, globalization, and pro-growth policies bestowing outsize rewards on the smartest and most resourceful. Returning to postwar marginal tax rates of 70% or higher, they say, would discourage innovation and hurt the economy.Ken Griffin, a hedge fund manager who madenewsin January by dropping $360 million on two abodes in London and New York, told Bloomberg News the following month that such tax hikes would represent attempts to “destroy the wealth creators of our society.”

Others see these types of proposals as necessary to address the economic and political distortions that lead to wealth stratification. In her campaign announcement, Warren described PresidentTrumpas “the latest and most extreme symptom of what’s gone wrong in America, a product of a rigged system that props up the rich and the powerful and kicks dirt on everyone else.” Even some billionaires have gotten the religion. In April,Ray Dalio, founder ofBridgewater Associates, the world’s largest hedge fund, called the widening U.S. economic divide a “national emergency” that, left unaddressed, will lead to “some form of revolution.”

Zucman sees ominous signs in the rise of the far right—the threat that has preoccupied him since he was a teenager on the streets of Paris. Inequality, he says, paves the way for demagogues. The causes he’s identified for the widening gap in the U.S. are a host of policy changes that started in the 1980s: lower taxes on the wealthy, weaker labor protections, lax antitrust enforcement, runaway education and health-care costs, and a stagnant minimum wage. America’s skyrocketing wealth disparity, he says, reflects that “it’s also the country where the policy changes have been the most extreme.”

When Reagan cut the top marginal tax rate from 70% to 28% across eight years, and later, when Presidents Bill Clinton and George W. Bush slashed tax rates for investors, they were doing so on the advice of economists. The prevailing belief, backed by theoretical models, was that lower taxes on the wealthy would stimulate more investment and thus more economic growth. The real world hasn’t been kind to those theories.

Since the era of liberalization and globalization began about 40 years ago, America’s economic growth has been markedly slower than it was the four decades prior. And though Zucman acknowledges that gross domestic product has risen faster in the U.S. than in other developed countries, he points out that the same is true of population. Measured in GDP per person or national income per adult, U.S. growth since 1980 is hard to distinguish from the pace in France, Germany, or Japan. Meanwhile, the typical worker wasbetter offabroad. From 1980 to 2014, for example, incomes for the poorest half of Americans barely budged, while the poorest half in France saw a 31% increase. “The pie has not become bigger” in the U.S., Zucman says. “It’s just that a bigger slice is going to the top.”

Share of Wealth Within Select Countries, 2014

Data: World Inequality Database

The actual effect of lower taxes on the rich, he argues, isn’t to stimulate the economy but to further enrich the rich and further incentivize greed. In his analysis, when the wealthy get tax breaks, they focus less on reinvesting in businesses and more on hiring lobbyists, making campaign donations, and pursuing acquisitions that eliminate competitors. Chief executive officers, for their part, gain additional motivation to boost their own pay. “Once you’ve created a successful business and the wealth is established and you own billions of dollars, then what these people spend their time doing is trying to defend that position,” Zucman says.

Even some inequality researchers question his and Saez’s proposal to restore postwar tax rates, though. Columbia University’s Wojciech Kopczuk, who once studied estate tax data with Saez, says citing inequality as grounds for such changes sounds “like an ex post facto justification of things you would want to do anyway.” The consequences of these policies, he notes, might include causing truly innovative entrepreneurs to lose control of their businesses. “Once you start naming these problems, you realize there are other solutions,” he says. He suggests the U.S. would be better off aggressively enforcing antitrust laws or tightening campaign finance laws.

Zucman says the response to inequality must be aggressive because wealth is self-reinforcing. The rich can always earn more, save more, and then spend more than everyone else to get their way. He considers Trump’s 2017 tax law—whichslashed rateson corporations, created a new deduction for business owners, and made the estate tax even easier to avoid—to be a textbook example. After decades of rising inequality and policies favorable to the top 0.1%, the U.S. delivered the rich a boatload of new goodies. “It’s hard not to interpret that as a form of political capture,” Zucman says.

Inside a Berkeley lecture hall in February, Zucman stepped 100 or so undergraduates through a few centuries of inequality, from slavery and the Industrial Revolution to the internet and climate change. Dressed in black, bearded, and pacing the front of the lecture hall, he approvingly quoted the classical 18th century economist Adam Smith on trade’s powerful impact on growth. This, he pointed out, is how countries such as China and South Korea pulled themselves up from poverty—an example of how at least one form ofinequality, between nations, was addressed.

For someone whose policy prescriptions are occasionally cast as radical, Zucman’s demeanor and rhetoric tend to the mild. He peppered the class with questions, urging reluctant undergraduates to offer their own explanations for economic history and stumbling briefly, despite his excellent English, over a student’s use of the expression “two heads are better than one.” He warned everyone that if the trends continue, their future could resemble the distant past.

In the slow-growing, hierarchical societies leading up to the 20th century, he said, the most important factor determining your economic prospects was the class into which you were born; from Italy to India, the poor stayed poor and the rich stayed rich. By the mid-20th century, though, the most crucial factor was the country of your birth. In the U.S. and Western Europe, rags-to-riches stories became common, if not routine. Maybe, Zucman warned, the 20th century was an egalitarian anomaly and inherited wealth would again dominate. The question, he said, is “how to have a meritocratic society when so much of wealth comes from the past.”

That day he also met with Saez to talk about a website the two were building. It had been a few weeks since Warren unveiled her wealth tax, and the men were creating a customizable tool to show the math underlying her proposal and let others formulate plans of their own. Saez mostly ran the meeting, but Zucman offered one suggestion: Give users the option of setting the rates as high as possible. Saez smiled and agreed.

Polls suggest that voters like Warren’s wealth tax, which would levy 2% on fortunes greater than $50 million and 3% on those higher than $1 billion. But the idea of taxing wealth, rather than income, alarms some policy experts and more than a few billionaires. Speaking on NPR,Howard Schultz, formerStarbucks Corp.CEO and a potential independent presidential candidate, called Warren’s proposal “ridiculous,” adding, “You can’t just attack these things in a punitive way.”

Others question how the government would value the assets of the rich, including their private businesses. Ideas such as Warren’s “work very poorly in practice,” Columbia’s Kopczuk says. “There is a reason why many countries get rid of wealth taxes.” At least 15 European countries have tried them; all but four haverepealedthem, most recently France.

Zucman responds that most European wealth taxes are poorly designed and that the practical issues can be resolved. For starters, such taxes must be created without loopholes allowing money to be stashed in trusts or offshore accounts. Then, with the legal regime in place, data technology could help tax collectors such as the IRS track and value wealth. A worldwide financial registry—or, failing that, the collection agencies—could require the rich to report all their transactions, exposing their holdings to scrutiny while providing the data needed to valuate similar assets. “Too many people just start from the assumption that it’s impossible,” he says.

The scope of the possible started widening after the financial crisis, as the U.S. and then the European Union moved to crack down on offshore shelters. The Panama Papers, a leak of millions of documents from a Central American law firm, pushed policymakers further. “We’ve won the argument,” says Alex Cobham, CEO ofTax Justice Network, an independent international advocacy group. “More or less everyone thinks banking secrecy should be finished.”

In recent months, Zucman has devoted a great deal of energy to the question of how multinational corporations avoid taxes. He’s produced papers and policy briefs showing that U.S. multinationals shift almost half of their overseas profits to five havens—Ireland, the Netherlands, Singapore, Switzerland, and the Greater Caribbean, which includes Bermuda. “That is a huge problem for the sustainability of globalization,” he says. Countries and territories are engaged in a race to the bottom, Zucman argues, offering ever-lower corporate rates in the fear that companies will shift their profits elsewhere. He proposes to “annihilate” such competition by apportioning profits based on where sales were made.

These ideas might be nonstarters today, but Zucman professes to take the long view. Remember, he points out, that the U.S. Supreme Court ruled the income tax unconstitutional in 1895; it took a constitutional amendment to legalize it in 1913. “There’s a lot of policy innovation ahead of us,” he says.

When Zucman and Saez’s site,wealthtaxsimulator.org, went live in March, it sparked some of that hoped-for innovation. One proposal, posted on Twitter by Adam Bonica, a political science professor at Stanford, was for a 100% tax on wealth beyond $500 million. He based it on what he called “Beyoncé’s rule,” which he explains as, “Think of the most talented and hardest-working person you know, and think about how much money they have and how much money they deserve.” Queen Bey, hetweeted, has an estimated net worth in the neighborhood of half a billion dollars. “Let’s have Howard Schultz explain to us why he should be worth more than Beyoncé.”