As Russia’s aggression in Ukraine escalates, so too have the deliberations in Europe and the United States over financial sanctions. It is only 48 hours, but it seems that we have come a long way since President Biden’s announcement on Thursday afternoon. As of the morning of midday Saturday 26 February east coast time, rumors were circulating of measures that would amount to a declaration of all-out financial warfare against Russia.

****

The debate is complicated and fast-moving and is driven by politics as well as technical argument. To sort things out, it is helpful to distinguish three questions.

Which entities are sanctioned.

What payment and communications methods are sanctioned.

What kind of purchases are sanctioned or not sanctioned.

A truly comprehensive sanctions regime, like that which the US has imposed on Iran, involves simultaneous and mutually reinforcing action on all three fronts. It entails action against both private banks and the national central bank, excision of financial institutions from both correspondent banking relationships and the SWIFT communications system, and targeted efforts to stop trade in strategic goods, if necessary by imposing secondary sanctions on those attempting to engage in trade with the sanctioned country.

By these means the US crippled Iran’s economy, reducing its Iran’s exports of oil from 2.5 million barrels a day to no more than 400,000. We are some way from that with regard to Russia.

***

So far in relation to Russia, the US has moved to stop US financial institutions from offering correspondent banking relationships to all major Russian commercial, industrial and policy banks. Crucially, it extended sanctions to Sberbank, by far the most important Russian bank.

The exclusion of a bank of Sberbank’s importance from the dollar financial system is a dramatic step.

This will have a disruptive effect on the ability of Sberbank to offer its clients any international service. As of today, February 26, VISA cards issued by Sberbank were no longer working outside Russia.

Sberbank’s stock value has crashed and will likely continue to plummet. The bank may be exposed to runs by Russian depositors anxious to get their hands on their cash and to switch it into foreign currency as quickly as possible.

Roughly half of Russian households have an account with Sberbank.

As Biden announced his measures on Thursday, European opposition was blocking any move to cut the Russian banks out of SWIFT, the Europe-based interbank communications system that links 11,000 banks worldwide. “European” opposition meant Germany and Italy both of which were concerned about paying their energy bills.

But, as far as energy concerned there was never any intention on the American part to interrupt payments. As I laid out in Chartbook #86, General License 8 exempts payments for energy, though those wishing to buy energy would need to find work arounds.

If the message was not clear enough, senior State Department energy security adviser, Amos Hochstein, later doubled down. The administration, he promised, had no intention of taking measures that would impact the oil market.

America is, at this point, not ready to sacrifice the interests of petrol buyers. Nor does the US oil industry like the idea of disruptive measures.

That was the state of play on Thursday.

***

Since Friday the indignation over Russian aggression, heroic Ukrainian resistance and the prospect that this will unleash an escalation of Russia’s attack, have raised the temperature in Europe. Not only are more and more European countries delivering weapons to Ukraine, including Germany, but there are calls to deliver such serious financial pain to Russia that it causes a change of mind on the part of Putin and his circle.

By Saturday midday European time, the German and Italian governments agreed to enter into talks about ending Russian access to the SWIFT system. Even the pro-Russian Hungarian government has indicated that it will not stand in the way.

As many people have pointed out, SWIFT is not the be all and end all. Eliminating access to SWIFT will further complicate any international transactions by Russian banks, but what will really cut them off is severing their relationships with correspondent banks. As Biden emphasized, the measures taken against Sberbank were more severe than cutting them out of SWIFT.

But excluding the Russian financial system from SWIFT will compound the pain it is already feeling.

As for energy, on Saturday the word out of Berlin was that the SWIFT exclusion would be selective. The clear suggestion is that there will be carveouts for energy payments.

SWIFT is a bulk messaging system, handling over 40 million communications per day to a total value of $5 trillion. Its appeal lies in its combination of efficiency and security. Neither efficiency nor security are of any immediate concern in paying for Europe’s energy. What is stake are daily payments to the tune of perhaps $600 million for oil and gas deliveries. The number of individual transactions is modest and can, if necessary, be handled in more direct and old-fashioned ways. For the purposes of paying Gazprom for gas deliveries, SWIFT is convenient but hardly essential.

If SWIFT-exclusion is implemented, it will deliver a severe blow to Russia’s financial institutions and indirectly to trade and confidence in the economy. It may have a ripple effect into the Belarusian financial system, which may act as a conduit for Russian payments and if so may find itself sanctioned as well.

As @edwardfishman and @jfriedlanderdc have explained, if Europe and the United States wish to hurt Russia more directly, they need to steel themselves to stop buying Russian oil and gas and then to consider whether they are willing to punish others for buying Russian oil and gas. According to estimates by Germany’s Kiel Institute of Economics, a Western embargo of oil and gas purchases would hit Russia’s economy by c. 4 percent. If secondary sanctions were applied - in effect a financial blockade of the Russian fossil fuel sector - the damage would be far more severe.

So far, neither option is on the table as far as energy is concerned.

What was rumored in Washington on Saturday morning were not more steps on energy, but a further escalation of financial measures: sanctions against Russia’s central bank.

***

Cutting Russia’s national bank out of the euro and dollar-based financial systems, would be a truly dramatic step that would strike at Russia’s national economy as a whole and one of Russia’s strongest cards, its foreign exchange reserves.

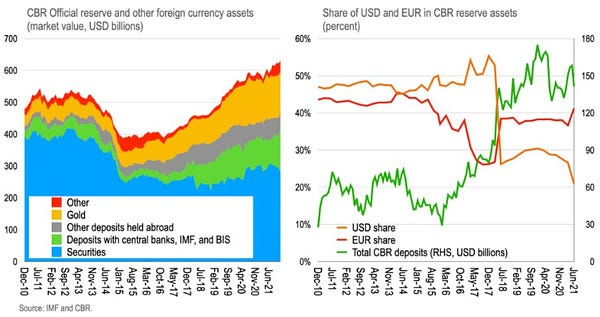

Russia has somewhere between $469 and $630 billion in foreign exchange reserves, depending on what you count.

Mark Copelovitch @mcopelov

People keep throwing around the $630B in reserves number about 🇷🇺. The relevant number is ~$469B. The rest is not liquid or readily available, as @anders_aslund explained in 2014: https://t.co/nYEpRrMZhi. Still large but far less & (again see the @PIIE piece) could go very fast. https://t.co/JsIrsADPKx https://t.co/zDvZKU70KLIn a conventional financial crisis these reserves provide an important cushion. They perform the same function in a scenario of limited sanctions - when sanctions are confined to individuals and businesses, as in 2014 for instance. I’ve regularly described them as the foundation of Putin’s autonomy in international affairs. That is how they worked both in 2008 and 2014 and Russia is not alone in pursuing this type of reserve strategy.

But, if Russia’s aggression provokes all-out financial war including sanctions against Russia’s central bank itself, then all bets are off. In such a scenario, the crucial question would be whether Russia can actually access its immense reserves and how it could spend them.

What is exposed is the degree to which any financial claims depend on a broader frame of legality and cooperation.

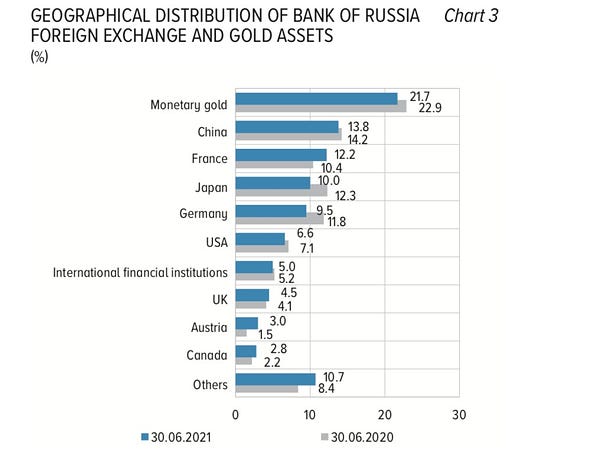

Russia has made sure not to hold a large fraction of its reserves in dollars or in the American financial system. Where exactly the funds are located has been the subject of considerable interest.

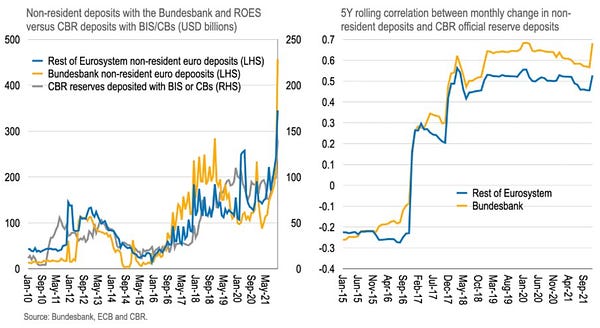

A more forensic investigation strongly suggests that a large amount may be stashed in Eurozone system, particularly with the Bundesbank.

Working from official publications, the brilliant @GeneralTheorist citing work by Zoltan Pozsar tracks the correlation between declared official deposits by the Central Bank of Russia and counterpart claims on the Euro system and the Bundesbank in particular. A high correlation is at least suggestive that the money that is moving is Russian.

This is by no means definitive, however. And at its next press conference this is THE question that the Bundesbank should answer is: How many deposits of the Central Bank of Russia do you hold? And will they be frozen immediately?

Russia also has a large reserve of gold. But what is the value of those reserves if the Russian central bank is deprived of access to international markets where it might sell the gold for euros or dollars? Russia would be reduced to bartering gold or other assets for whatever imports Russia needs, cutting out the need for international currencies. Which partners would be willing to engage in such a trade and at what price?

China is the only likely candidate and they would dictate stiff terms. But, as keen market observers note, difficulties with payments mean that Russian oil is already trading at discounts.

In short, sanctions against Russia’s central bank would be tantamount to full-scale financial war. The prospect evokes memories of the chaos of the 1990s.

Alex Nice @AlexNicest

I think a key point about Russian financial stability is that in previous shocks, such as 2014 oil price plunge, we didn’t see massive pressure on deposits and demand for dollarisation. That could change (if I were a Russian I’d be buying cash dollars now) https://t.co/si9XLMR3QpWould energy be exempt in such a scenario?

It seems hardly plausible. Of course, it might be possible to arrange some kind of carveout. But would Russia be willing to supply oil and gas to customers engaged in such extreme financial punishment. It seems more than unlikely.

Indeed, Sony Kapoor has argued that since Russia is likely to cut off gas supplies imminently, the West should move first.

***

The situation in Ukraine is clearly critical. Days matter. As investors weigh the scale of the likely damage, financial markets in Moscow are becoming dramatically disturbed. On Friday as the markets gained the impression that sanctions might not be a severe as, at first, feared, the cost of ensuring Russian debt against default actually fell.

At this point it remains an open question, how far either Europe or the United States are willing to go.

But if the West does want to keep up the pressure on Russia and materially to assist the Ukrainian struggle for survival, it needs to ramp up its measures. The packages announced on Thursday and Friday were tantamount to accepting defeat. If the West wants to punish Russia comprehensively, it has the means to do so. The cost will be far less than the huge sacrifice born by Ukraine, but, if energy is involved, the cost may be significant, and it will certainly hurt not just the elite, but a large part of Russian society. It is a major step.

Nenhum comentário:

Postar um comentário