Irlanda: o desconforto da riqueza

Paulo Roberto de Almeida

Brasília, 8 de fevereiro de 2005.

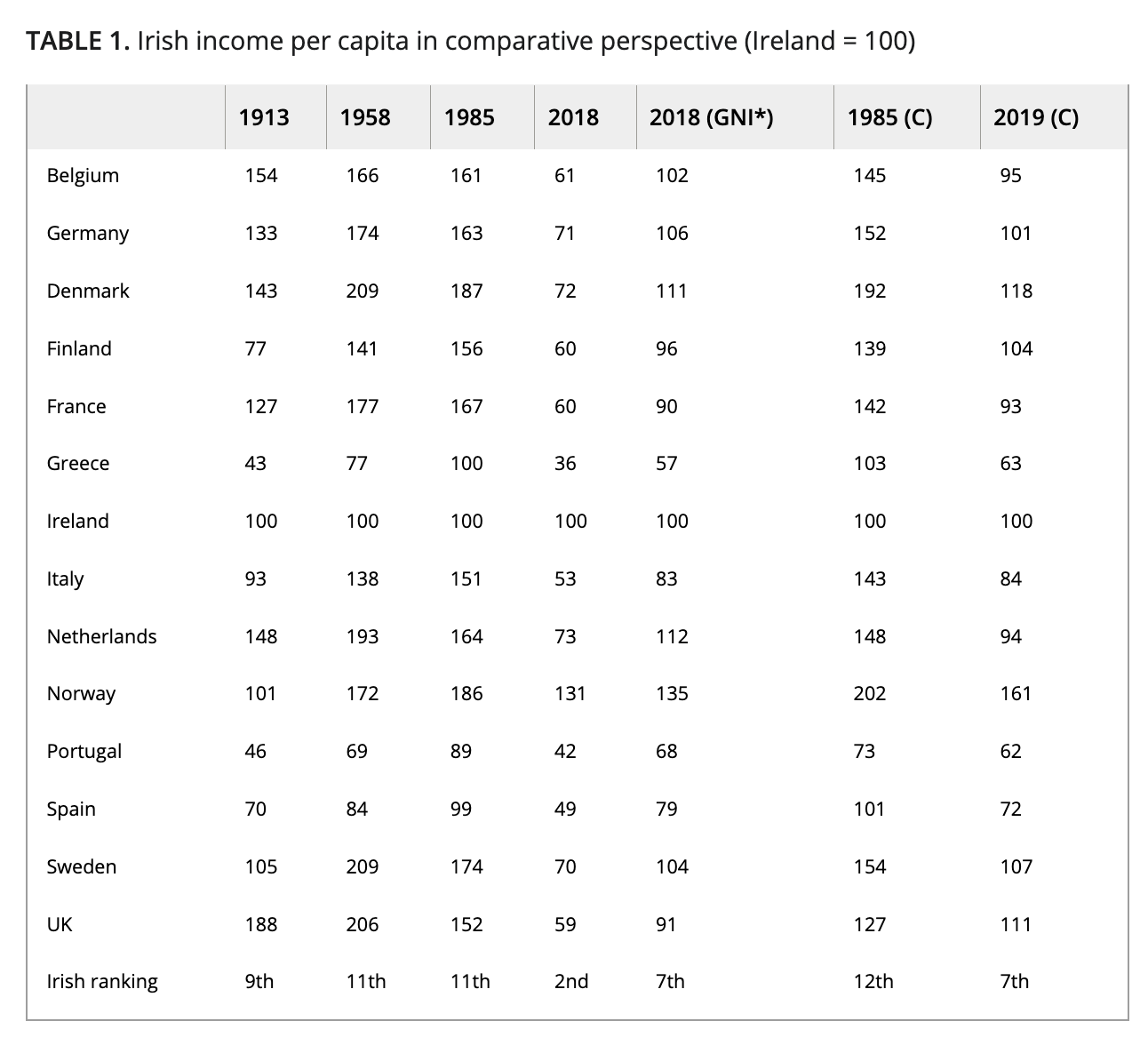

A Irlanda foi um dos países que mais cresceu nos últimos vinte anos. Partindo de patamares muito baixos de desenvolvimento – não considerando aqui a tradição secular de “exportação” de irlandeses por motivos de miséria econômica –, os progressos econômicos obtidos pela Irlanda foram particularmente impressionantes na última década do século XX, depois que o país se organizou para enfrentar os desafios de sua integração à Europa comunitária e à abertura de mercados prometida pelo Ato Único de 1986, que previa um mercado unificado em 1992. Entre 1991 e 2001, o PNB cresceu à média de 6,4% ao ano em termos reais, alcançando a média européia em 2003 (em termos de PIB, o crescimento foi ainda maior, pois o PIB per capita supera a média da UE em 15%, mas é preciso considerar que a Irlanda é um país de atração de investimentos estrangeiros, por excelência, o que diminui, portanto, o seu PNB em relação ao PIB). Ao mesmo tempo, o desemprego crônico, que existia anteriormente, foi sensivelmente reduzido, passando de uma média de 15% da PEA a menos de 4% no mesmo período.

Esses resultados se devem, segundo a análise de Marialuz Moreno Badia, do Departamento da Europa do FMI (boletim do FMI de 31 de janeiro de 2005, disponível no link: http://www.imf.org/external/pubs/ft/survey/spa/2005/013105S.pdf), à aplicação de políticas econômicas corretas, como a abertura comercial, a participação na UE e ao contexto econômico externo favorável. Em especial, o ingresso na união econômica e monetária da UE suscitou um forte decréscimo das taxas de juros reais e estimulou o investimento direto estrangeiro. A consolidação fiscal reduziu a dívida pública, que passou de 100% do PIB em 1988 para apenas 36% em 2001, e criou espaço para reformas tributárias que ampliaram os investimentos e o emprego.

A Irlanda pode estar vivendo hoje uma situação similar à da Holanda no século XVI, segundo a análise histórica de Simon Schama (The Embarassment of Riches), quando os holandeses dispunham de bastante conforto material, a ponto de poderem se entregar a luxos antes proibitivos, como o investimento em arte, em conforto pessoal e até em especulações em bolsa (como provado pela “febre das tulipas”, que provocou um dos primeiros estouros de “bolha financeira” já estudados pelos historiadores econômicos). Segundo um artigo recente na imprensa americana, os irlandeses poderiam estar vivendo uma “crise de identidade”, pois nunca antes tinham desfrutado de tal nível de vida.

Em face dessa crise de identidade, como poderíamos situar o Brasil, com o seu “desconforto da miséria”? Segundo o presidente, a miséria atingiria algo como 44 milhões de brasileiros (ou 11 milhões de famílias, aquelas mesmas que ele pretende alcançar mediante o programa Fome Zero, englobado no Bolsa Família). A primeira providência para uma comparação objetiva entre esses dois “desconfortos” antitéticos seria analisar as causas da pobreza em ambos os países e as estratégias adotadas para superá-la. Ao que se conhece, a Irlanda não colocou em vigor nenhum programa de “alívio da fome”, embora tenha conhecido, no passado, episódios dramáticos de fome epidêmica, que determinaram a saída de centenas de milhares de irlandeses para outros países, os Estados Unidos em especial.

O que a Irlanda fez, de verdade, foi ter decidido, pouco mais de duas décadas atrás, tornar-se um país desenvolvido. Para fazê-lo, ela tomou o caminho mais rápido, que não é o da distribuição de dinheiro para quem é pobre ou dispõe de rendimentos mínimos. Ela o fez, basicamente, pela via da educação nacional, a única rota segura para a elevação dos padrões de produtividade do trabalho humano, que por sua vez ainda é o caminho mais rápido para a elevação dos níveis de renda e de bem-estar material. O projeto nacional dos irlandeses foi assim, tão simplesmente, dar uma educação de qualidade a cada um dos seus filhos, prolongando a formação nas etapas técnico-profissional e depois universitária. Por certo, isto não foi tudo: eles também liberalizaram a economia e se abriram ao capital estrangeiro: de fato a Irlanda foi um dos países da Europa que mais recebeu investimento direto estrangeiro, em proporção do PIB, nos três últimos lustros. Esse investimento veio para a Irlanda porque tinha certeza de que iria encontrar um ambiente de negócios favorável e de que a mão-de-obra seria adequada para os empreendimentos relativamente sofisticados – geralmente na indústria eletrônica – que iriam ser estabelecidos.

E quanto ao Brasil, o que poderíamos dizer? O diagnóstico e, sobretudo, os prognósticos não são os mais favoráveis. Nossa mão-de-obra dispõe de escassos 4,3 anos de estudo, na média (contra algo como 9 anos para um operário coreano), o que é simplesmente inaceitável do ponto de vista do capitalismo moderno. O ambiente de negócios não é exatamente aquele que mais atrai investidores: segundo o Banco Mundial, o prazo médio para se abrir uma empresa vai a mais de 150 dias, e o de fechamento então se perde no horizonte do tempo. Encargos trabalhistas, contribuições previdenciárias, impostos diretos e indiretos, custo dos serviços que devem ser terceirizados, condições precárias de logística, intervencionismo excessivo e regulacionismo estatal exagerado são apenas alguns dos obstáculos que se antepõem a um ritmo sustentado de crescimento e expansão para qualquer empresário que se arrisca a tentar negócios no Brasil.

Temos, ao que parece um longo caminho pela frente antes de nos livrarmos do atual “desconforto da miséria”. Esta, em sua faceta mais extrema, não é exatamente devida à ausência de condições materiais para que a sociedade possa manter um processo sustentado de redistribuição de renda, mas mais exatamente à falta de qualificação geral de capacidade produtiva da maior parte da mão-de-obra, o que vale dizer, em primeiro lugar, de ausência de formação educacional dessa mesma população. O único projeto nacional que faz sentido, no Brasil, é o de um pacto pela qualidade do ensino. Assim, em lugar do “fome zero”, deveríamos estar pedindo “educação dez”.

Paulo Roberto de Almeida

é sociólogo e diplomata.

(pralmeida@mac.com; www.pralmeida.org)