Um discurso importante de Macron. Resumo: ele quer mais subvenções estatais e mais protecionismo. Não se sabe se ambas as medidas são sustentáveis na ausência de maior produtividade europeia. Um cul-de-sac como diriam os franceses.

BBC NEWS BRASIL

As inundações no Rio Grande do Sul —que provocaram mais de cem mortes e vem afetando milhões de gaúchos — serão um dos momentos definidores da Presidência de Luiz Inácio Lula da Silva, segundo análise da agência Bloomberg.

Nos últimos dias, vários veículos da imprensa internacional destacaram as enchentes no sul do Brasil.

A análise da Bloomberg fala em "teste crucial para a liderança de Lula".

"Os assessores [de Lula] dizem que ele está perfeitamente consciente de que este pode ser o seu 'momento Katrina', uma referência ao furacão de 2005 que pegou o presidente dos EUA, George W. Bush, desprevenido e entrou no vocabulário global como sinônimo de fracasso de liderança em uma crise", afirma o texto da Bloomberg, assinado por Travis Waldron

A agência disse que Lula reagiu às enchentes com atendimento às necessidades básicas dos afetados, viajando à região e assinando um decreto que retira os gastos emergenciais das regras fiscais.

"Com mais chuva e temperaturas em queda previstas durante a semana, os desafios só vão aumentar", diz o texto da Bloomberg.

"Isso pode dar a Lula a oportunidade de recuperar uma presidência assolada nos últimos meses por rivalidades internas, brigas com o Congresso, escrutínio do mercado sobre os seus planos de gastos e popularidade em declínio."

A Bloomberg diz que Lula foi eleito na esteira da insatisfação da população com a gestão do governo de Jair Bolsonaro durante a pandemia de Covid-19 —e que este momento das enchentes pode definir se Lula vai reconquistar sua liderança no país, ou perdê-la de vez.

O jornal britânico Financial Times destacou o prejuízo financeiro do Estado —estimado na ordem de R$ 5 bilhões.

"O Rio Grande do Sul é a quinta maior economia do Brasil e é um importante produtor agrícola e um centro industrial", diz a reportagem de Bryan Harris e Michael Pooler.

"O Estado é responsável por 70% da produção nacional de arroz, e acredita-se que 10% tenham sido perdidos devido às cheias. Prevê-se também que 30% da colheita de soja do Estado, de 21 milhões de toneladas, pereça. Lula disse que o Brasil importará arroz e feijão do exterior para evitar a escassez de alimentos."

O texto também cita críticas do professor Pedro Luiz Cortês, da USP, às autoridades brasileiras: "Os governos estadual e federal estavam mal preparados para essas emergências climáticas".

'DÍVIDA HISTÓRICA'

Na quarta-feira (8/5), dia em que o número oficial de mortos chegou a cem, o jornal americano New York Times publicou uma reportagem chamada, em tradução livre, "Imagens de uma cidade brasileira embaixo d'água" — com fotos e relatos das pessoas afetadas.

"O Brasil está enfrentando uma das piores enchentes da história recente. Chuvas torrenciais inundaram o Estado do Rio Grande do Sul, no sul do país, onde vivem 11 milhões de pessoas, desde o final de abril e provocaram graves enchentes que inundaram cidades inteiras, bloquearam estradas, romperam uma grande barragem e fecharam o aeroporto internacional até junho."

A reportagem de Ana Ionova e Tanira Lebedeff narra o drama de alguns dos afetados que conseguiram ser resgatados.

"Muitos dos que ficaram isolados aguardavam ajuda nos telhados. Alguns tomaram medidas desesperadas para fugir: quando o abrigo onde sua família estava inundada, Ana Paula de Abreu, 40 anos, nadou até um barco de resgate enquanto segurava seu filho de 11 anos debaixo do braço. Dois moradores de um bairro de Porto Alegre usaram um colchão inflável para retirar pelo menos 15 pessoas de suas casas inundadas."

O New York Times cita Mercedes Bustamante, professora da Universidade de Brasília, que diz que "os efeitos do El Niño [nas inundações no Rio Grande do Sul] foram exacerbados por uma combinação de alterações climáticas, desmatamento e urbanização desenfreada".

Em entrevista à BBC News Brasil, Bustamante disse que a região agora afetada é uma área "onde vamos viver muito mais extremos, segundo os modelos climáticos".

O Washington Post, principal jornal da capital americana, também noticiou as enchentes.

"Mesmo em um país cada vez mais habituado a desastres naturais provocados pelas alterações climáticas, as inundações que engoliram o Rio Grande do Sul — um dos Estados mais desenvolvidos e prósperos do Brasil — abalaram gravemente esta nação de 215 milhões de habitantes. Com mais da metade das cidades do Estado enfrentando enchentes [...], o Rio Grande do Sul não foi apenas afetado. Foi arrasado."

A reportagem de Terrence McCoy e Marina Dias diz que, apesar de alertas sobre os efeitos das mudanças climáticas feitos por alguns políticos e cientistas brasileiros, "a retórica produziu poucas mudanças concretas".

"Em um comentário feito exclusivamente ao The Washington Post, Lula atribuiu a devastação no Rio Grande do Sul às falhas da comunidade global em responder às mudanças climáticas. Ele disse que existe uma 'dívida histórica'. Os países mais pobres que historicamente emitiram poucos gases com efeito de estufa, disse ele, estão sofrendo com a poluição das nações mais ricas."

Lula disse ao Washington Post: "Esta foi a terceira enchente recorde na mesma região do país em menos de um ano. Nós e o mundo precisamos nos preparar todos os dias com mais planos e recursos para lidar com eventos climáticos extremos."

Enviado pelo dileto amigo Tomas Guggenheim:

Xi Jinping’s China is not nearly the unstoppable economic powerhouse that many predicted.

One of the things I try to avoid when writing this newsletter is getting too far over my skis on any particular subject. Bold predictions or declarations of victory might produce clicks at the ol’ take factory, but they can quickly prove foolish and do more harm than good in the longer term. For these and other reasons, I’ve hesitated to talk too much about China’s very rough 2023.

But the year’s almost over, the data are piling up, and … almost nobody in Washington seems to notice (at least not publicly).

Indeed, if you were to pick up a newspaper (just go with it) and turn to the politics section, you’d think that China was an unstoppable economic juggernaut destined to dominate the world at the expense of a fading United States and other Western democracies. Just yesterday, in fact, the House Select Committee on the Strategic Competition between the United States and the Chinese Communist Party released a big report decrying the CCP’s “multidecade campaign of economic aggression against the United States and its allies”—one that used an “intricate web of industrial policies” and other state planning to “achieve dominance in global markets” and “increase U.S. dependency on PRC imports”—and thus recommending a broad array of new U.S. trade/investment restrictions and subsidies (along with some decent stuff, too) to respond to this urgent economic threat.

Meanwhile, in that same (hypothetical!) newspaper’s business section, you’d see a much, much different China—one that’s struggling economically, thanks in no small part to many of the very same economic policies the Select Committee is freaking out about. Maybe someone could let them know?

China’s Economy Is in Rough Shape—Thanks in No Small Part to Chinese Government Policy

Back in late 2022, the general consensus was that the Chinese economy would surge in 2023 following the Chinese government’s sudden abandonment of its disastrous “Zero COVID” policy. For the first couple months at least, the consensus appeared to be correct: Growth, consumption, investment, and other metrics surged as China’s economy reopened and things returned to (sorta) normal. That rally proved to be short‐lived, however, and signs of economic trouble—both short‐term and long—have emerged almost everywhere you look.

And it’s increasingly clear that Chinese government policies warrant much of the blame.

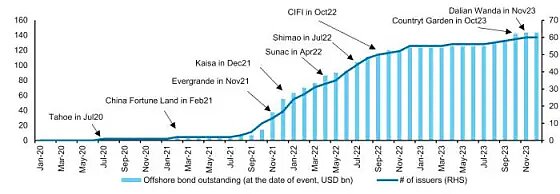

The biggest and most obvious problem lies in China’s property sector, which has long been distorted by government policy and has struggled mightily since the high‐profile collapse of behemoth developer Evergrande. According to investment bank Barclays, the Financial Times reports, “More than half of China’s top developers followed Evergrande into default after Beijing moved in 2020 to restrict new borrowing, unravelling a funding model that was built on dollar‐denominated high‐yield debt and bankrolled by local government financing vehicles.” As the following chart shows, dozens Chinese property firms (right Y axis)—with more than $140 billion in outstanding dollar‐denominated debt (left Y axis)—have now defaulted:

Meanwhile, many provinces in China are struggling under the weight of reckless debt—both public and hidden—accumulated during China’s boom years. The IMF estimates that “off‐balance‐sheet government debt” ranges somewhere between $7 trillion and $11 trillion—thanks in large part to so‐called “local‐government financing vehicles” (LGFVs) that borrowed gobs of money to build infrastructure or fund other local projects and companies at central planners’ prodding.

“No one knows what the actual total is,” the Wall Street Journal adds, “but it has become abundantly clear over the past year that local governments’ debt levels have become unsustainable,” with as much as $800 billion now at a “high risk” of default. China’s Finance Ministry, to its credit, told local governments to “borrow more responsibly” in the future. However, because those same governments are also under pressure from the central government to report strong economic growth (a common authoritarian move, as we’ve previously discussed), they disregarded the ministry’s advice and instead “went on another borrowing spree.” Thus, by the end of last month, “the outstanding bonds of their financing vehicles ballooned to more than twice what it was in 2018.” Oops.

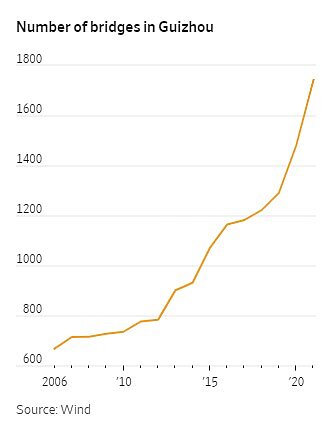

All this spending and debt raises several long‐term economic concerns. For starters, the actual value of the local government projects at issue is increasingly in question—as is the past GDP growth it generated. Tales of useless and empty structures funded by Chinese government debt abound. “A high‐speed rail station in Danzhou,” the WSJ reports, “cost $5.5 million to build but was never put into use because passenger demand was so low.” In debt‐ridden Guizhou, meanwhile, a single state‐owned company built 24 of the world’s 100 highest bridges (including the world’s highest) in the province, and “by the end of 2019, the total length of Guizhou’s highways was the fourth‐longest in the country, topping some of the wealthier provinces like Guangdong and Zhejiang.” All that debt and construction contributed to Guizhou’s eye‐popping 9.5 percent annual GDP growth from 2011–2022, but now the bill is coming due—and, as one Chinese credit analyst put it, “Eventually, someone must pay for it.”

That “someone” gets to the second debt problem: Analysts increasingly believe that China’s central government will have to step up and take on large amounts of new debt to pay for the provinces’ reckless spending (which Beijing, of course, encouraged). For this and related reasons, Moody’s Investors Service recently downgraded China’s credit rating to negative from stable, “because the country is likely to provide more support to financially stressed local governments and state‐owned enterprises.” That’s not only a reputational black eye for the CCP but will also make borrowing more costly in the future.

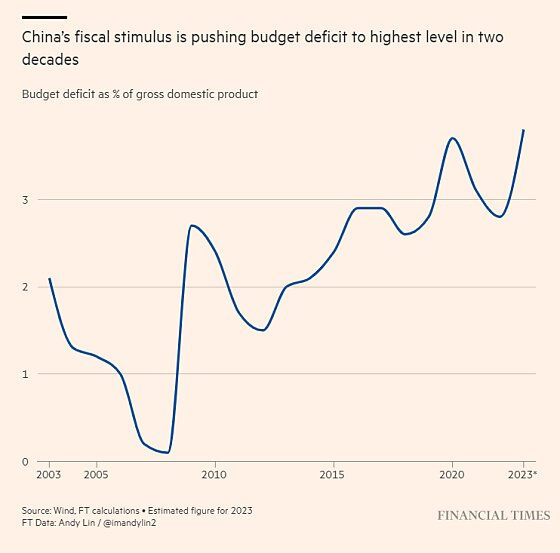

Third, all this debt and overinvestment could mute future government efforts to stimulate the economy via fiscal policy—even if Beijing technically has room on its (public) balance sheet to do so. From the WSJ:

“The leading point is they are running into diminishing returns in building stuff,” [Harvard economist Ken Rogoff] said, “There are limits to how far you can go with it.”

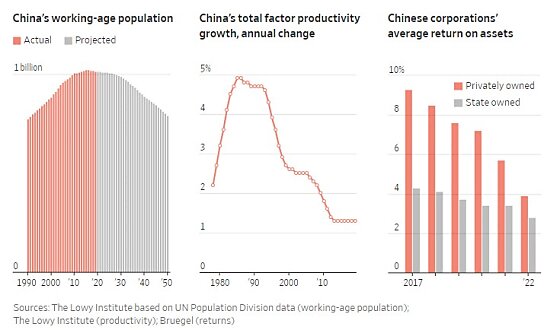

With so many needs met, economists estimate China now has to invest about $9 to produce each dollar of GDP growth, up from less than $5 a decade ago, and a little over $3 in the 1990s.

Returns on assets by private firms have declined to 3.9% from 9.3% five years ago, according to Bert Hofman, head of the National University of Singapore’s East Asian Institute. State companies’ returns have retreated to 2.8% from 4.3%.

This “pushing on a string” problem, combined with concerns about tepid tax revenues and off‐book debts, has caused many analysts to “question just how much budgetary firepower Beijing really has to boost flagging confidence and drive stronger economic momentum”—even though China has stepped up spending in response to recent economic turmoil.

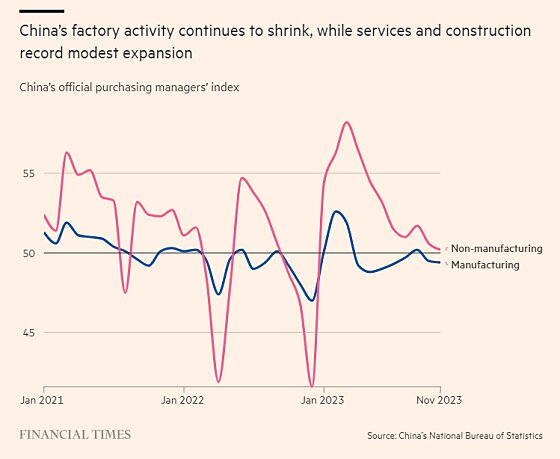

China’s much‐vaunted manufacturing sector, meanwhile, may be suffering from similar problems. Chinese governments have subsidized numerous “strategic” sectors like steel, shipbuilding, and electric vehicles, but—thanks to lagging domestic and global demand and increasing geopolitical tensions (often caused by those same subsidies!)—they may have no place to sell it. As a result, the sector has teetered this year between mild expansion and (more often) contraction:

Meanwhile, non‐manufacturing industries just hit “the lowest reading since China was swept by Covid last December.”

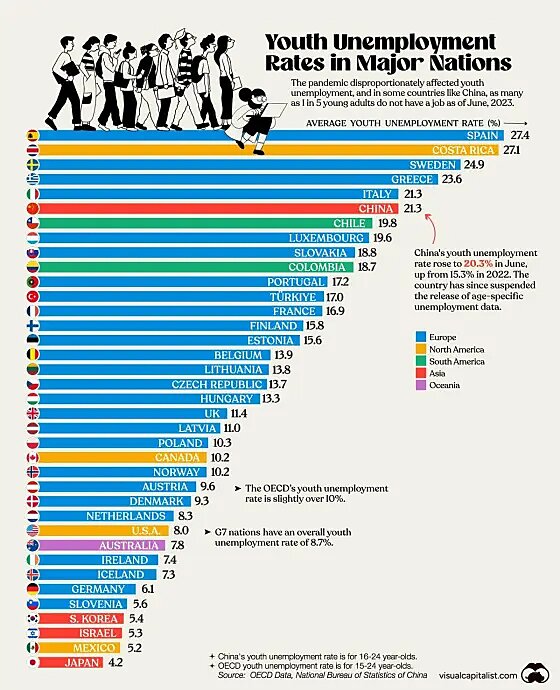

Outside the corporate sector, other problem signs have emerged. Most notably, the youth unemployment rate hit a record high of 21.3 percent in June … right before the government ceased to publish the official number. (Always a good sign!) Add students to the total, and the rate could be 46.5 percent. Shockingly, nixing the stat didn’t make the problem go away: As the WSJ’s Josh Zumbrun writes, social media reports and independent data show that youth unemployment remains a “troubling story” in China, even if we can’t pin down exactly how troubling it is. Meanwhile, one private forecaster’s “measure of job openings began to plunge in May, and as of early December was 35 percent lower than a year earlier—not a great sign in an economy desperately trying to absorb huge numbers of jobless youth.” Assuming the rate is still hovering around those June levels, it’d be one of the highest in the world:

One of the issues here, the New York Times notes (along with many others), is a policy‐driven mismatch between the types of young workers China’s planners once wanted its education system to produce (college grads to work in services or government) and the “strategic” industries the government is currently supporting (which need factory workers trained primarily at vocational schools). Thus, for example, “The number of teenagers entering vocational and technical high schools plummeted 25 percent between 2010 and 2021,” while “about 60 percent of the Chinese population turning 18 enroll at a university”—up from 10 percent in 2000. Now, China’s burgeoning EV industry faces “a shortfall of skilled technicians as young people shun manufacturing careers.”

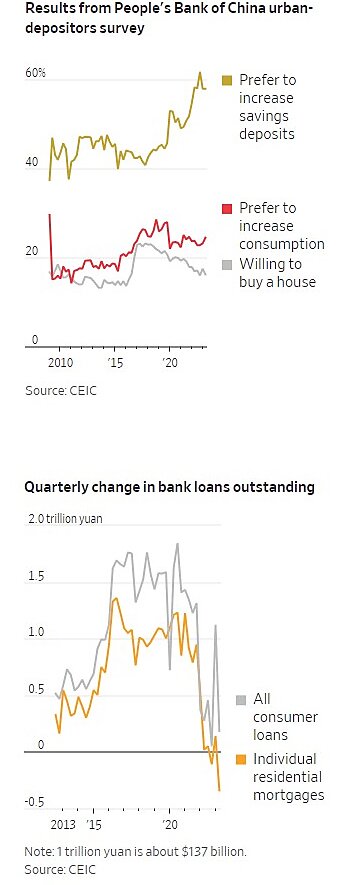

Problems are not, however, isolated among China’s young. As the Peterson Institute’s Adam Posen documented in August, Chinese households seem to have lost confidence in the future of the Chinese economy and government. As a result, they are saving more—a lot more—and consuming less: Compared with 2015, bank deposits (as a share of GDP) are up by 50 percent and remain elevated, while consumption of durable goods has declined by about one‐third. Private investment (down two‐thirds since 2015) shows a similar insecurity.

WSJ’s Nathanial Taplin came to a similar conclusion a couple weeks later after looking at a different set of consumer survey and loan data: “Beijing has failed to convince households that their financial future is secure in the post‐Covid era.”

Unless the CCP focuses more on consumption and less on “grandiose industrial policy and geopolitics,” Taplin adds, a “painful period of economic stagnation” might be ahead. He and Posen are certainly not alone in their diagnoses and warnings.

Other signs of household stress have since emerged. Earlier this month, we learned that “defaults by Chinese borrowers have surged to a record high … highlighting the depth of the country’s economic downturn and the obstacles to a full recovery.” Making matters worse is Chinese law, which requires these 8.5 million people to be “officially blacklisted” and thus “blocked from a range of economic activities, including purchasing aeroplane tickets and making payments through mobile apps such as Alipay and WeChat Pay, representing a further drag on an economy plagued by a property sector slowdown and lagging consumer confidence.” Lower incomes and higher costs, meanwhile, have caused China’s massive state health insurance system to lose tens of millions of subscribers in 2022—an “unprecedented” decline that, after years of growth, is expected to continue this year.

Structural Headwinds and ‘Japanification’?

Other, longer‐term headwinds also remain problematic, as I first documented here back in 2021 and as my Cato colleague Clark Packard recently updated in an essay for our ongoing globalization project. Along with debt, China’s demographics (low birth rates, a rapidly aging population, shrinking workforce, etc.), difficulty attracting and retaining both homegrown and global talent, and stagnating economic dynamism and productivity pose further challenges to future economic growth, government budgets, and political stability.

Combine these headwinds with the shorter‐term issues, and the narrative around China has shifted radically in the last year. Analysts once attracted to (or worried about) strong growth are suddenly reversing course and worrying about excess capacity and stagnation. Unlike most other big economies, in fact, China is now grappling with deflation: Consumer prices went negative in July, returned there in October, and declined even more last month, indicating that a brief late‐summer revival may have been a “dead‐cat bounce.” Producer prices, meanwhile, have been negative for a full year.

Perhaps most troubling for the Chinese economy is the fact that these problems have arisen despite “a slew of supportive measures from Beijing to boost sentiment and growth since mid‐2023.”

Pushing on a string, indeed.

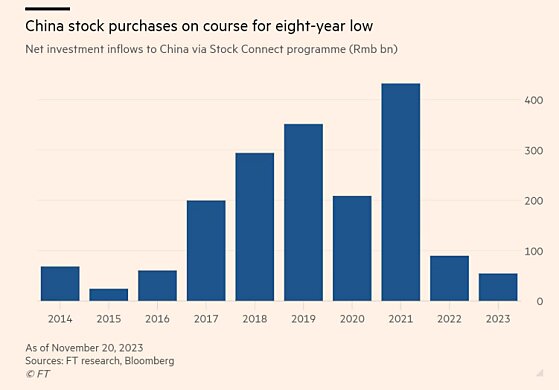

None of this means that China is on the verge of an all‐out economic collapse or anything, but investors have significantly revised their bets on the Chinese economy. As of late November, “more than three‐quarters of the foreign money that flowed into China’s stock market in the first seven months of the year has left, with global investors dumping more than $25bn worth of shares despite Beijing’s efforts to restore confidence.”

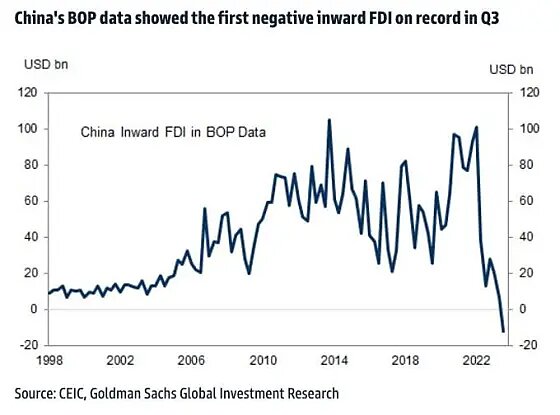

And foreign direct investment is fleeing China in ways not seen in decades—not just slowing their investments there but “now ditching Chinese investments and pulling money out at a remarkably rapid pace” for the first time ever.

If these FDI trends continue for the rest of the year, the FT’s Robin Wigglesworth adds, “China is on track to attract less FDI than Poland did in 2022, and less than half of what Sweden did”—and, he notes, even that might be too optimistic.

As a result, many analysts who once confidently predicted China’s economy would soon overtake the United States’ have lowered their growth projections, extended their timelines, or even ditched them altogether. Now, commentators openly wonder if China will be the “next Japan,” meaning a rapidly growing economy once predicted to supplant the United States, but instead—thanks to high levels of debt and state‐directed economic distortions combined with slower growth and demographic and external pressures—ends up facing not just a few months or even a year of economic malaise but decades:

Some economists see alarming parallels between China’s current predicament and the experience of Japan, which struggled for years with deflation and stagnant growth. In the 1990s, a collapse in stock markets and real‐estate values in Japan pushed companies and households to drastically cut back spending to service burdensome debts—a so‐called balance‐sheet recession that some see taking shape in China today.

As one analyst recently put it this summer: “When the real estate bubble started collapsing last year, all these Chinese economists began to worry about a Japan‐like situation where so many people are paying down debt all at the same time and [the] economy could then fall into a deflationary spiral. I think that is actually already happening in China.” The latest deflation data would appear to confirm his fears (at least for now).

Beyond the aforementioned debt and deflation similarities between the two nations, there are plenty of others: banking, property, demographics, a high‐savings/investment economic growth model, and policy‐driven malinvestment and overcapacity (especially in manufacturing and infrastructure). It’s not a stretch to think that China’s economic engine will be sputtering for years to come, much like Japan’s did decades ago.

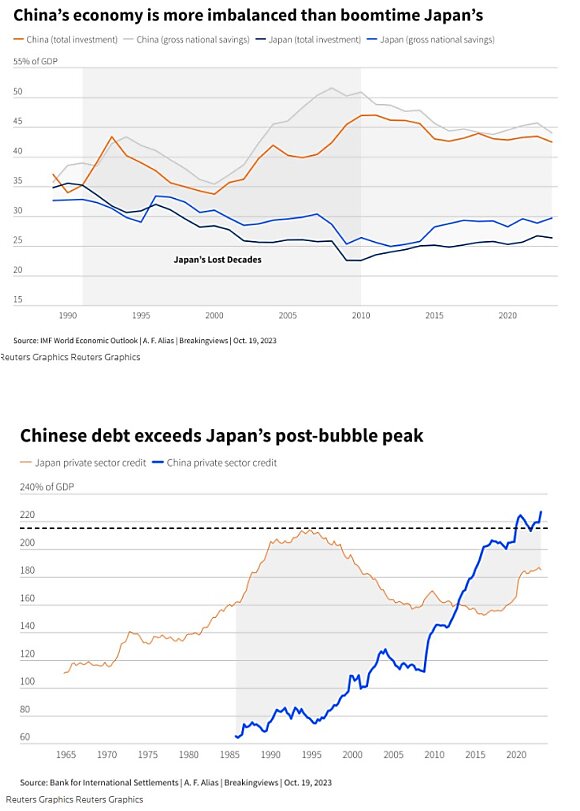

In fact, China’s situation is in many ways worse than Japan’s was when it began to stall. For starters, China is still relatively poor:

China’s national income per person reached about $12,850 last year, below the current threshold of $13,845 that the World Bank classifies as the minimum for a “high‐income” country. Japan’s per capita national income in 2022 was about $42,440, and the U.S.’s was about $76,400.

China’s economic imbalances are also bigger than Japan’s were in 1990, as are its total debts (that we know of!):

As Goldman‐Sachs notes, China’s demographics headwinds also are bigger than Japan’s were in the 1990s, and its housing sector weakness is “more pronounced” too. Japan also didn’t pursue its own version of China’s wasteful and ineffective Belt & Road Initiative. And instead of backing off the economic meddling like Japan eventually did, China’s now leaning in:

Guided by a desire to strengthen political control, Xi’s leadership has doubled down on state intervention to make China an even bigger industrial power, strong in government‐favored industries such as semiconductors, EVs and AI.

While foreign experts don’t doubt China can make headway in these areas, they alone aren’t enough to lift up the entire economy or create enough jobs for the millions of college graduates entering the workforce, economists say.

Just yesterday, in fact, China’s top central planners “vowed to make industrial policy their top economic priority next year,” thus letting down investors who were hoping the government would shift away from “technology self‐reliance” toward more pro‐growth policy instead.

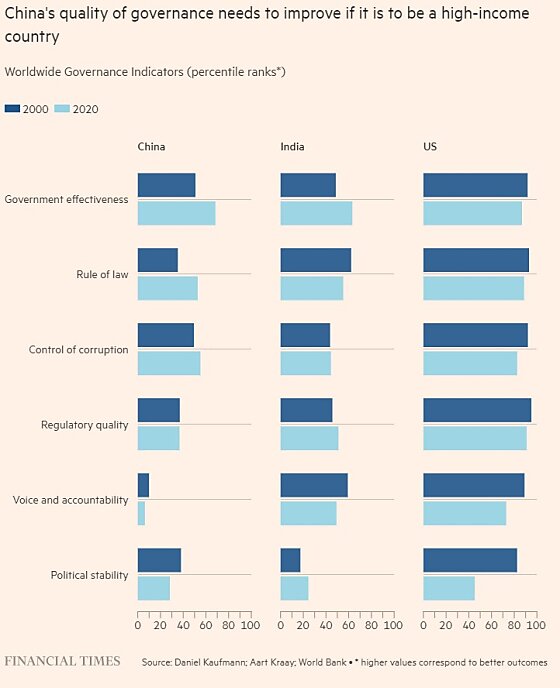

Finally, there are the negatives raised by China’s political system, aside from the much‐publicized corruption and institutional shortcomings (see chart below). As discussed last year, for example, authoritarian regimes have informational problems from both the bottom up (e.g., local governments distorting facts/data to avoid punishment) and the top down (e.g., the central government doing the same to make its regime look good). Autocratic systems also provide government officials with the mechanisms to forcibly restrict countervailing data (e.g., youth unemployment), which can distort government and private sector decision‐making and discourage foreign investment. Posen adds that authoritarian regimes have a long history of starting out strong (fed by government largesse) but inevitably intervene in the economy in “increasingly arbitrary” ways—ways that boost uncertainty, cause households and businesses to hoard cash and avoid risk, and persistently slow economic growth. Once this cycle gets going, it’s difficult to reverse without fundamental reforms, none of which appear to be on China’s horizon.

So, far from being fueling prosperity, Chinese state capitalism and autocracy could be an anchor in ways Japan never had to deal with.

Summing It All Up

Despite all the similarities and my own personal biases, I remain reluctant to embrace China’s “Japanification” narrative for numerous reasons. Most notably, China today fundamentally differs from 1990s Japan in ways—politics, foreign policy, level of government intervention in the economy, human rights issues, sheer size—that make this cross‐country comparison even more difficult than such analogies usually are. And, it should be noted, many of the same analysts talking about “Japanification” are quick to follow with notes about how China might avoid Japan‐style stagnation because its economy today is in some ways better off than Japan’s was in 1990, and because the Chinese government has more “policy space” to act. The precise direction of China’s future economy—lost decade, slower‐but‐steady growth, full‐on collapse, or something else—remains unclear.

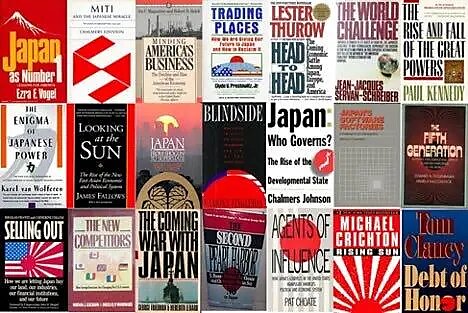

What is clear today, however, is that Xi Jinping’s China is not nearly the unstoppable economic powerhouse that many believed it to be—and wanted the United States to copy—just a short time ago. (See, for example, Cass, Atkinson, Prestowitz, Rubio, Dalio, and Kerry/Khanna to name just a few.) There again lies another parallel with Japan: as R Street’s Adam Thierer documented in 2021 (and as us geezers can recall firsthand), Japanese industrial policy and planning once caused many American wonks and policymakers to predict Japan’s inevitable economic dominance and to propose all sorts of U.S. subsidies and protectionism in response. People wrote books and made movies about the “Japan threat,” and implored Washington to copy Tokyo’s economic model:

That dominance, of course, never materialized. Indeed, just as those books were being published (written by some of the same folks screeching about China today, by the way), Japan was beginning its long period of economic stagnation, with the Japanese government years later admitting that its vaunted economic model was a big part of the problem.

China might not follow the exact same path as Japan, but it sure does seem to be heading in the same general direction. And as we discussed a few months back, there are already plenty of signs that China’s industrial policies aren’t nearly the big winners some have claimed. (More have since emerged, by the way.) One can be forgiven for missing the warning signs in that some of us saw years ago through the fog of positive Chinese economic data. Dire warnings today, however, deserve much less sympathy—and attention.

Hopefully Congress will give them what they deserve.

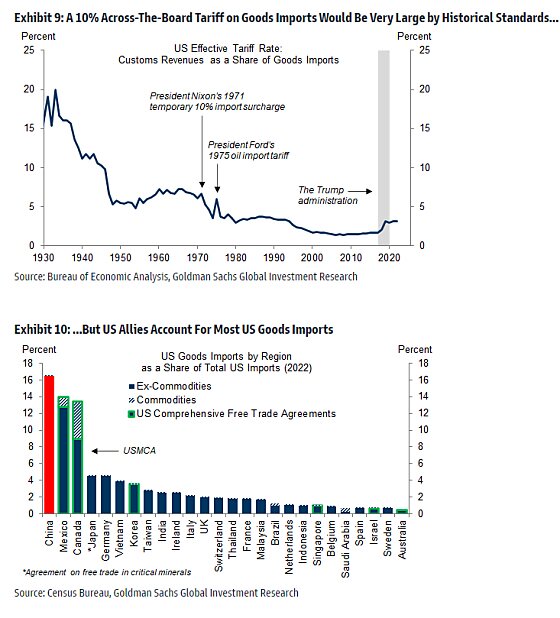

Chart(s) of the Week

Trump wants historically large tariffs on (mainly) U.S. allies:

"O Rio Grande do Sul enfrenta um momento trágico, após chuvas intensas que atingiram o estado entre o fim de abril e o começo de maio. Os estragos sem precedentes exigem respostas emergenciais, coordenação do poder público e mobilização da sociedade civil.

O quadro calamitoso também exige uma série de reflexões. Quando os governos vão priorizar a prevenção, em vez de apenas reagir a desastres? Até quando setores da classe política vão insistir no negacionismo climático? Por que flexibilizar a legislação ambiental ainda recebe apoio? O que motiva algumas pessoas a espalhar mentiras que tumultuam a ajuda aos atingidos pelas enchentes?

Nesta newsletter, o Nexo traz mapas sobre a situação gaúcha, textos em que especialistas analisam as questões listadas acima, além de podcasts que relatam o drama de quem luta para obter água potável, tendo de conviver com o medo de saques e violência."

O embaixador Jorio Dauster propõe uma espécie de gestão compartilhada, com todos os países latino-americanos, na hipótese do exercício efetivo do Brasil no CSNU, se e quando ele for admitido na condição de novo membro permanente, caso ocorra a reforma da Carta da ONU e a ampliação do seu principal órgão decisório (o que atualmente parece bastante difícil).

A Argentina, que sempre se opôs a essa candidatura, talvez concorde com essa "solução", ou expediente, para remediar sua contrariedade, o que também é uma hipótese.

É uma proposta conciliatória, que talvez tenha boa repercussão entre os pequenos países latino-americanos, o que parece improvável entre os grandes, que vão, provavelmente, insistir na tese da rotatividade, ou seja, uma cadeira permanente, mas para a região, não para um país.

Existe um erro no artigo de Jorio Dauster, ao proclamar que os cinco membros permanentes do CSNU eram "potências nucleares", quando eles eram apenas os vencedores, a China e a França com muitas dificuldades, pois que tiveram de ser ajudadas pelas duas potências ocidentais. Como lembrou Ricardo Seitenfus, a nuclearização dos cinco membros foi em datas diferidas, os EUA inclusive só depois, efetivamente, de assinada a Carta da ONU.

Estados Unidos, 1945

URSS, Rússia, 1949

GB, 1952

Franca, 1960

China, 1964

A miragem do "bilhete de ingresso" no CSNU via armamento nuclear foi durante muito tempo entretido pelos militares brasileiros e até por vários diplomatas, alguns deles até chegando a considerar o FHC um "traidor da pátria", por ter feito o Brasil aderir ao TNP em 1996. Ora, recorde-se que a China e a França só aderiram ao TNP no início dos ANOS 1990!

Paulo Roberto de Almeida

Brasília, 9/05/2024

O Brasil no Conselho de Segurança da ONU

Jorio Dauster, Embaixador aposentado, consultor de empresas e tradutor

A inoperância do Conselho de Segurança das Nações Unidas ao ser defrontado com os trágicos conflitos na Ucrânia e em Gaza trouxe de novo ao debate público a questão de sua reforma. Na verdade, esse é um tema que remonta praticamente à criação da ONU, uma vez que o órgão supostamente encarregado da manutenção da paz foi sempre tolhido pelo exercício do poder de veto por um ou mais de seus membros permanentes. Até março do corrente ano, a Rússia (e antes a União Soviética) usou o poder de veto 128 vezes; os Estados Unidos, 85 vezes; o Reino Unido, 29 vezes; a China, 19 vezes; e a França, 16 vezes.

Mais recentemente, após serem vetadas diversas propostas sobre Gaza, o Conselho de Segurança, em 25 de março último, aprovou unanimemente uma resolução (com a abstenção dos Estados Unidos) exigindo o cessar-fogo imediato entre Israel e o Hamas, bem como a libertação imediata e incondicional de todos os reféns. Apesar dessa rara concordância, em que pela primeira vez os Estados Unidos não vetaram uma decisão rechaçada por Israel, a guerra continua sem nenhuma trégua e sem a entrega de qualquer refém.

Malgrado esse retrospecto decepcionante, ou antes devido a ele, a necessidade de reforma do sistema destinado a salvaguardar a paz mundial se torna cada vez mais urgente diante da exacerbação das tensões em vários pontos do globo. De fato, a composição do Conselho de Segurança reflete a configuração de poder presente no fim da Segunda Guerra Mundial, espelhando as condições excepcionais de que dispunham então as cinco potências nucleares.

No entanto, de lá para cá, inclusive em consequência do gradual enfraquecimento da hegemonia norte-americana e da emergência de outras potências, em especial da China, é natural que se busque novos arranjos mais compatíveis com a multipolarização em curso. Ao longo das últimas décadas, várias reformas já foram sugeridas, inclusive uma apresentada há quase 20 anos conjuntamente por Brasil, Índia, Japão e Alemanha, pela qual esses quatro países se tornariam membros permanentes (sem poder de veto) e seriam criados ainda mais dois assentos permanentes (para países africanos) e quatro não permanentes. Obviamente, todas as diversas propostas de reforma têm encontrado diferentes tipos de oposição, sendo, inclusive, conhecidas as posturas da Argentina contra a pretensão brasileira, a da China contra a presença do Japão, a dos Estados Unidos contra a entrada da Alemanha.

Entretanto, cabe persistir embora pareça pouco produtivo que o Brasil simplesmente reitere as reivindicações que faz há pelo menos três décadas. Assim, com vistas a injetar um sopro novo nesse debate até hoje infrutífero, sugiro que o Brasil, sem abdicar da candidatura à condição de único membro permanente da região, ofereça aos outros 32 países da América Latina e do Caribe, caso eleito, a possibilidade de participarem efetivamente das deliberações do Conselho de Segurança ampliado. Com isso, se estaria reconhecendo de modo implícito que os debates conducentes ao alargamento do Conselho deram caráter irrevogavelmente "regional" à futura representação dos países em desenvolvimento, inclusive no caso da África em que, ao contrário da posição reconhecidamente excepcional de que gozam o Brasil e a Índia em suas respectivas regiões, nenhum país ostenta condições idênticas a desses dois.

Em sintonia com os princípios que regem a política externa do governo do presidente Lula, o mecanismo proposto deve ser apresentado como exemplo de democratização das relações internacionais, objetivo advogado por nós e por numerosas nações latino-americanas desde os primórdios da ONU. Serviria assim tanto para atenuar a frustração dos países que não seriam membros permanentes quanto para aumentar a adesão à causa do Brasil pelos países médios e pequenos da região.

Como o objetivo desse novo mecanismo consistiria em permitir o amplo envolvimento dos 32 países associados nos trabalhos do Conselho de Segurança sob a liderança e a coordenação do Brasil, deveria ser estabelecido um sistema de consultas sistemáticas em Nova York com as representações de tais países acerca dos itens constantes da pauta daquele órgão. Por fim, de modo a garantir a efetiva coparticipação dos associados nas matérias levadas a voto, o Brasil lhes submeteria o projeto definitivo de resolução e, dentro de prazos compatíveis com a mecânica decisória do Conselho, receberia suas indicações de "voto virtual": sim, não ou abstenção. Inexistindo consenso devido à posição divergente de três ou mais associados, o Brasil se absteria. Caso o projeto de resolução fosse rejeitado pelo Brasil ou pela maioria dos associados, a posição de todos na região seria explicitada em declaração de voto feita pela delegação brasileira.

Sem dúvida essa ideia pode e deve ser trabalhada pelos meus colegas na ativa, mas estou convencido de que, além de ser superior ao conceito de rotatividade dos novos membros permanentes, pode facilitar as acomodações em outros continentes caso também adotada por eles. Eventualmente, poderíamos então contar com uma frente sólida de 152 nações em desenvolvimento para pressionar pela imprescindível reforma do Conselho de Segurança.

Trecho de seu artigo na The Atlantic deste mês, "The Propaganda War":

“In 2013, as Chinese President Xi Jinping was beginning his rise to power, an internal Chinese memo, known enigmatically as Document No. 9—or, more formally, as the Communiqué on the Current State of the Ideological Sphere—listed “seven perils” faced by the Chinese Communist Party. “Western constitutional democracy” led the list, followed by “universal human rights,” “media independence,” “judicial independence,” and “civic participation.” The document concluded that “Western forces hostile to China,” together with dissidents inside the country, “are still constantly infiltrating the ideological sphere,” and instructed party leaders to push back against these ideas wherever they found them, especially online, inside China and around the world.

(…)

This is the core problem for autocracies: The Russians, the Chinese, the Iranians, and others all know that the language of transparency, accountability, justice, and democracy appeals to some of their citizens, as it does to many people who live in dictatorships. Even the most sophisticated surveillance can’t wholly suppress it. The very ideas of democracy and freedom must be discredited—especially in the places where they have historically flourished.“

(...)

The Atlantic, may 8, 2024

Chamada para publicação de dossiê na Revista Carta Internacional v. 19, n. 3 de 2024

A Carta Internacional, revista científica de Relações Internacionais da Associação Brasileira de Relações Internacionais (ISSN 2526-9038) está selecionando artigos para o Dossiê "As múltiplas crises do internacional: transição, hegemonia e resistência nas ruínas da ordem global”."

A revista aceita artigos inéditos em português, espanhol ou inglês. O prazo máximo de submissão para o dossiê é 31 de maio de 2024.

Dossiê:

As múltiplas crises do internacional: transição, hegemonia e resistência nas ruínas da ordem global

Editores: Carolina Moulin (UFMG) e Daniel Maurício de Aragão (UFBA)

TEXTO

“O velho está morrendo e o novo não pode nascer; neste interregno, uma grande variedade de sintomas mórbidos aparece”. A frase de Antonio Gramsci, tema do IX Encontro da ABRI em 2023, revela o espírito do tempo presente e as inquietações e incertezas que perpassam a análise da ordem internacional contemporânea. Múltiplas ‘patologias de crise’ – guerras, epidemias, catástrofes ambientais, genocídios, desigualdades aprofundadas, populismos reacionários e fissuras nas formas democráticas de governo, para citar apenas algumas – tem reverberado um sentimento de “fim de mundo”. Esses sintomas mórbidos resvalam nas dificuldades das estruturas e instituições globais, erigidas na esteira do projeto moderno liberal, de se adaptarem e, no limite, se reinventarem sob outros termos diante das demandas das sociedades atuais, face ao capitalismo financeirizado, às transformações na relação entre ordens internacionais, formas de Estado e forças sociais (Cox, 1981) e de crise de hegemonia (Fraser, 2020).

Sobre o húbris do projeto da modernidade liberal - agravada pelo fracasso de sua vertente fundamentalista, o neoliberalismo, e por retrocessos associados à sua crise, particularmente no que tange à democracia e aos direitos humanos e à ascensão do autoritarismo e conservadorismo; por crises recorrentes dos processos de acumulação capitalista; por promessas frustradas nos processos de globalização e integração regional; por conflitos, guerras e pandemias - Estados e as Organizações Internacionais têm dificuldade de reagir. Ao mesmo tempo, protestos e formas de resistência apontam para fissuras e novas possibilidades de rearticulação, ainda que efêmeras, tentativas e provisórias. Dos protestos globais às ocupações, passando por hashtags e táticas efusivas de mobilização, emergem conformações alternativas à relação entre ordem e justiça, violência e poder, representação e política e entre o local e o internacional, com implicações importantes para o futuro da disciplina de Relações Internacionais.

Para o dossiê, almejamos receber contribuições que se engajem com esses “sintomas mórbidos”, seus impactos e alternativas, seus limites e aberturas. Os editores convidam artigos que aprofundem debates sobre essa conjuntura histórica, em temas tais como:

- Crise de hegemonia, seus atores e processos;

- Crise do capitalismo associada às transformações dos processos de acumulação, agravada pela especulação do capital financeiro e por processos de expropriação e precarização;

- Limitações, retrocessos, incógnitas e alternativas nos e aos processos de globalização e integração regional;

- Limites e possibilidades teóricas nas Relações Internacionais, refletindo sobre a resiliência de abordagens tradicionais e pluralismo teórico no campo enquanto estratégias possíveis para compreensão de processos políticos do mundo atual;

- Reflexões substantivas e originais sobre noções de crise e catástrofe enquanto gêneros importantes para a disciplina de RI, na esteira da centralidade de fenômenos como conflitos armados, pandemias, e esgotamento de modelos de desenvolvimento ancorados no capitalismo liberal e suas consequentes formas de institucionalização;

- Contribuições sobre estratégias narrativas e transdisciplinares que possibilitam olhar para temas persistentes das Relações Internacionais (guerra e paz, mobilidade e circulação, exclusão e desigualdade, populismo e nacionalismo, dentre outros) de forma criativa e imaginativa em um contexto de transição;

- Perspectivas de futuro nas Relações Internacionais, a partir, principalmente, das reivindicações de movimentos antirracistas, feministas, LGBTQIAPN+, socio ambientalistas, quilombolas e indígenas, bem como das reações e reconfigurações, usualmente violentas dos modos de governo e governança sobre esses territórios de luta política e social.

Regras de submissão:

O formato dos artigos deverá seguir o padrão já adotado pela revista:

1. O artigo deve ser inédito e redigido em português, inglês ou espanhol. Além de inédito, o artigo não deve estar em apreciação concomitante em nenhum outro periódico ou veículo de publicação, no todo ou em parte, no idioma original ou traduzido.

2. Os artigos devem ter entre 7500 e 8500 palavras, incluindo título, resumo e palavras-chave (em português, inglês e espanhol), notas de rodapé e referências bibliográficas.

Site da revista: https://www.cartainternacional.abri.org.br/Carta/announcement/view/9

Um outro texto que eu comecei a escrever no dia do 1o. turno da eleição presidencial em 2018, mas não terminei e nunca divulguei. Divulgando hoje um texto incompleto e inédito, talvez eu possa ter vontade de levar adiante e fazer algo não conectado a eleições.

Paulo Roberto de Almeida

Brasilia, 7 de maio de 2024

O sentido da política externa

Paulo Roberto de Almeida

Brasília, 3 de outubro de 2018

Uma política externa sólida e confiável toma apoio, antes de mais nada, em uma política doméstica igualmente sólida e confiável, ou seja, estável, com objetivos de largo prazo e dotada de meios para se sustentar nos planos interno e externo. Essa base é dada por alguns elementos estruturais consistentes: (a) uma macroeconomia consistente, capaz de promover um processo de crescimento sustentado, num ambiente de negócios aberto e competitivo, nos marcos de uma democracia de mercado de boa qualidade, com uma governança responsável e transparente; (b) funcionamento pleno de instituições respeitadas, especialmente a Justiça, para reduzir os custos de transação em benefício dos setores que produzem empregos e renda para a população; (c) um sistema educativo de boa qualidade, inclusivo, podendo contribuir para o sistema de inovação e ganhos de produtividade e de competitividade, num ambiente mundial cada vez mais integrado; (d) abertura a comércio e investimentos estrangeiros, sem discriminação.

Qual o papel da política externa no contexto brasileiro? Seu papel sempre foi o de coadjuvar o processo de desenvolvimento, mas geralmente no quadro de políticas nacionalistas, autonomistas, protecionistas, em lugar de buscar inserir o Brasil no mundo, seguindo orientações de abertura econômica e de liberalização comercial. Os antigos parâmetros que permitiram ao Brasil uma industrialização bem-sucedida, ainda que com distorções e deformações derivadas daquela antiga atitude econômica, já não correspondem mais aos requerimentos das novas características da economia mundial e não podem fazer o Brasil avançar para outras etapas de seu processo de modernização.

(Incompleto; inédito)

Paulo Roberto de Almeida

Brasília, 3 de outubro de 2018

Meu mais recente livro – que não tem nada a ver com o governo atual ou com sua diplomacia esquizofrênica, já vou logo avisando – ficou final...